Target Acquisition Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

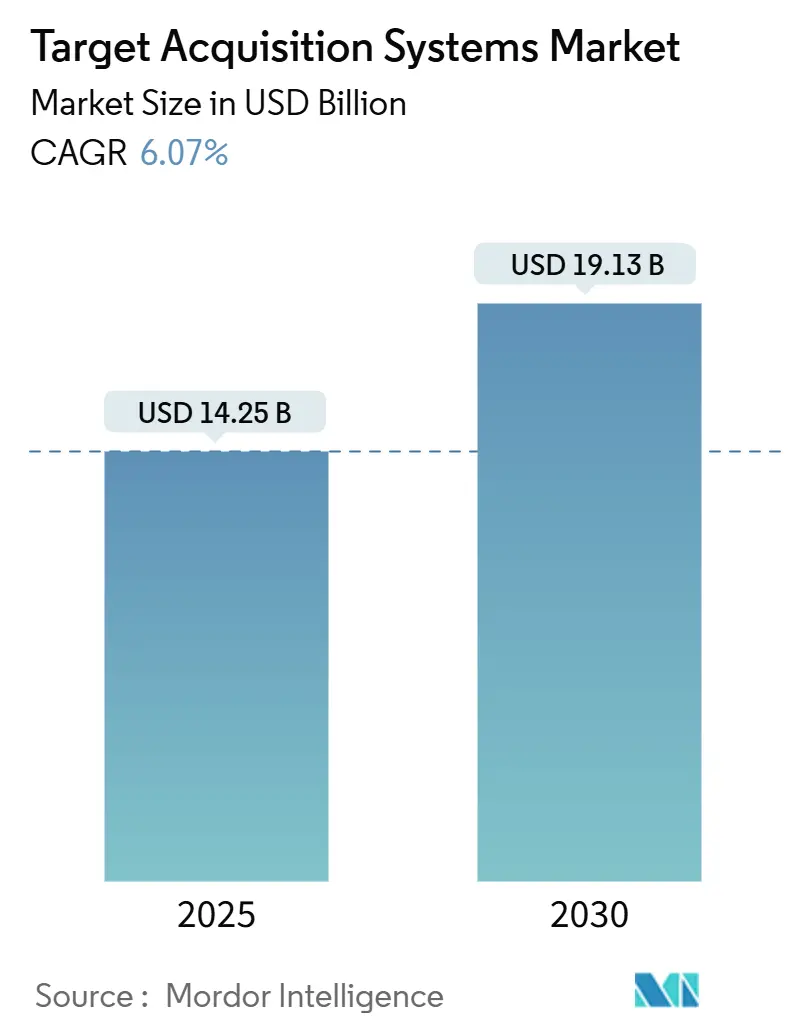

| Market Size (2025) | USD 14.25 Billion |

| Market Size (2030) | USD 19.13 Billion |

| Growth Rate (2025 - 2030) | 6.07% CAGR |

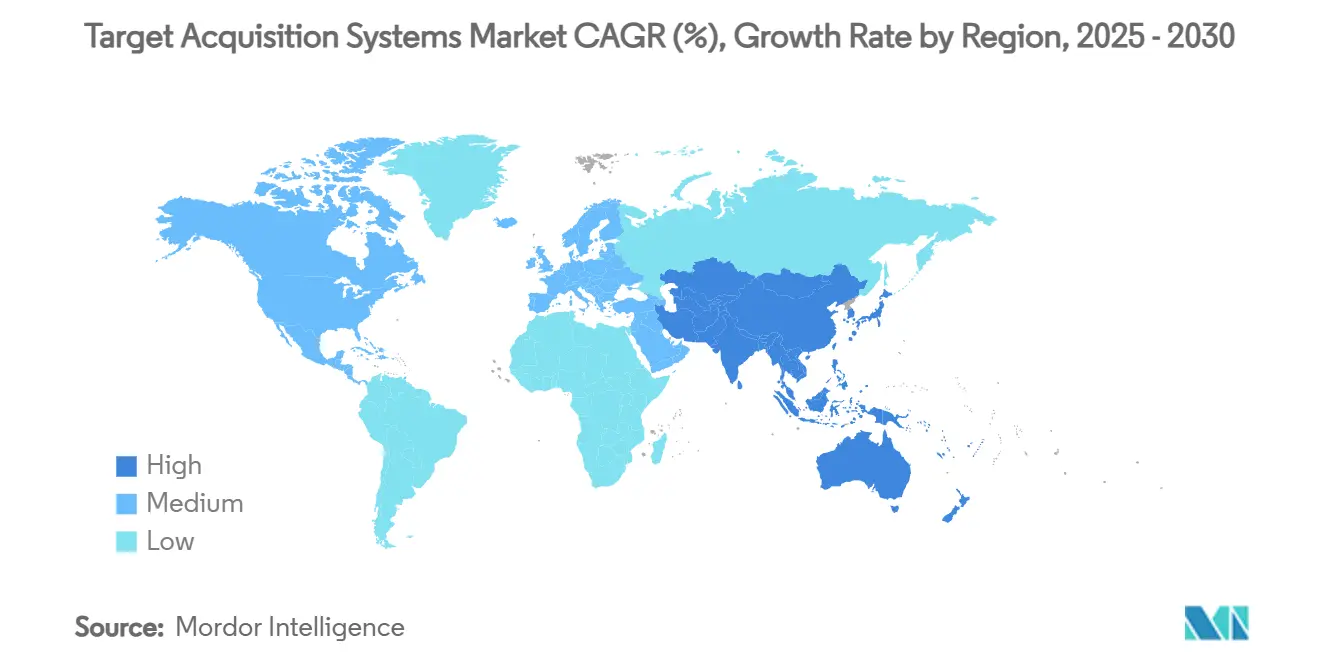

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

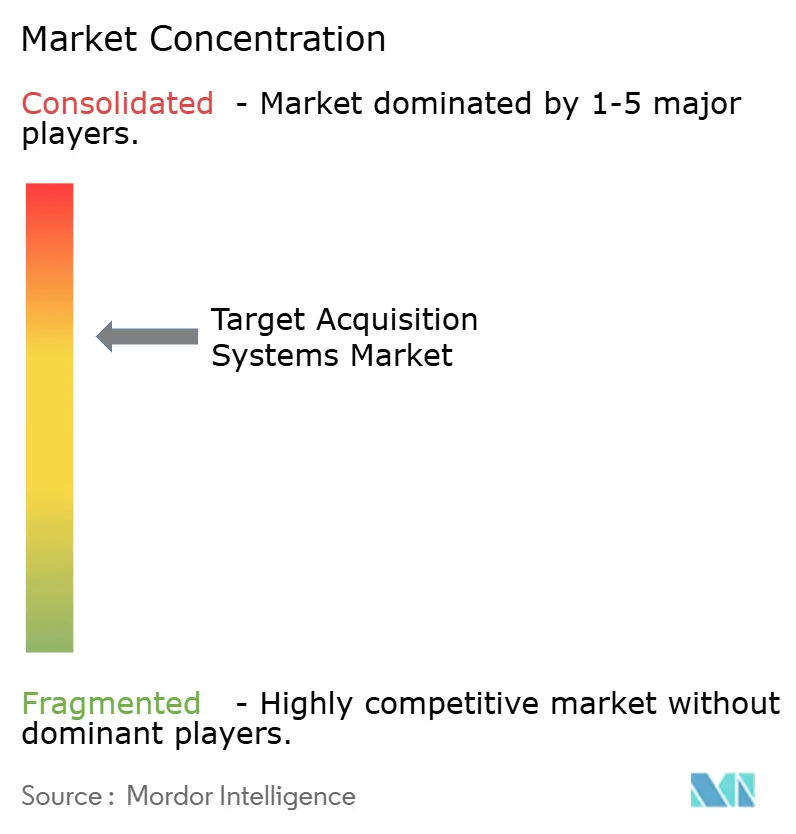

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Target Acquisition Systems Market Analysis by Mordor Intelligence

The target acquisition systems market size is estimated at USD 14.25 billion in 2025 and is forecasted to expand to USD 19.13 billion by 2030 at a 6.07% CAGR. Heightened geopolitical tensions and the spread of unmanned aerial threats have pushed governments to accelerate force-modernization programs, especially those aimed at network-centric operations. NATO members have pledged to keep annual defense outlays above the 2% of GDP threshold, ensuring a dependable funding stream for new detection, tracking, and fire-control technologies. Land platforms hold the widest installed base, yet airborne systems are growing fastest as armies demand persistent, multi-domain surveillance. Electro-optical/infrared (EO/IR) sensors retain the largest share, although rapid adoption of AI-enabled multi-sensor fusion suites is reshaping competitive dynamics. Thanks to major US programs, North America remains the biggest regional spender, while Asia-Pacific leads growth because of record budgets in China, Japan, and India.

Key Report Takeaways

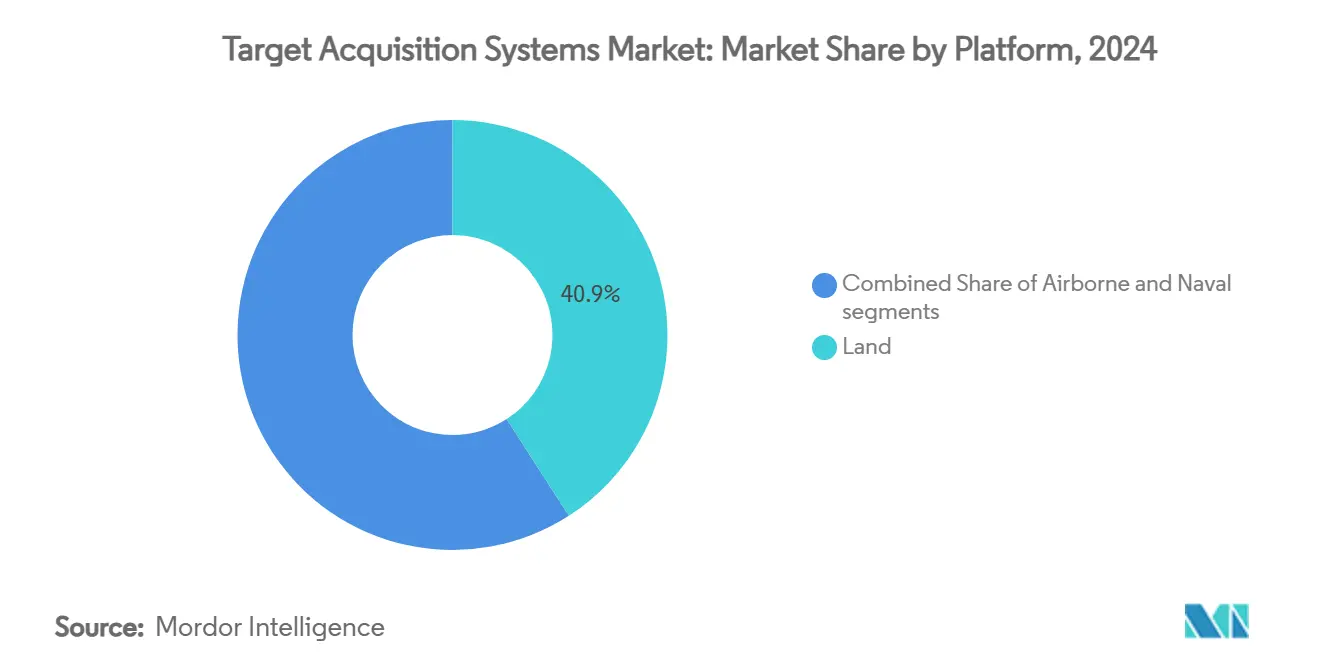

- By platform, land systems led with 40.90% of the target acquisition systems market share in 2024; airborne systems are projected to post the quickest 8.23% CAGR through 2030.

- By sensor type, EO/IR products accounted for a 42.17% revenue share in 2024, whereas multi-sensor fusion suites are expected to grow at a 7.26% CAGR over the same period.

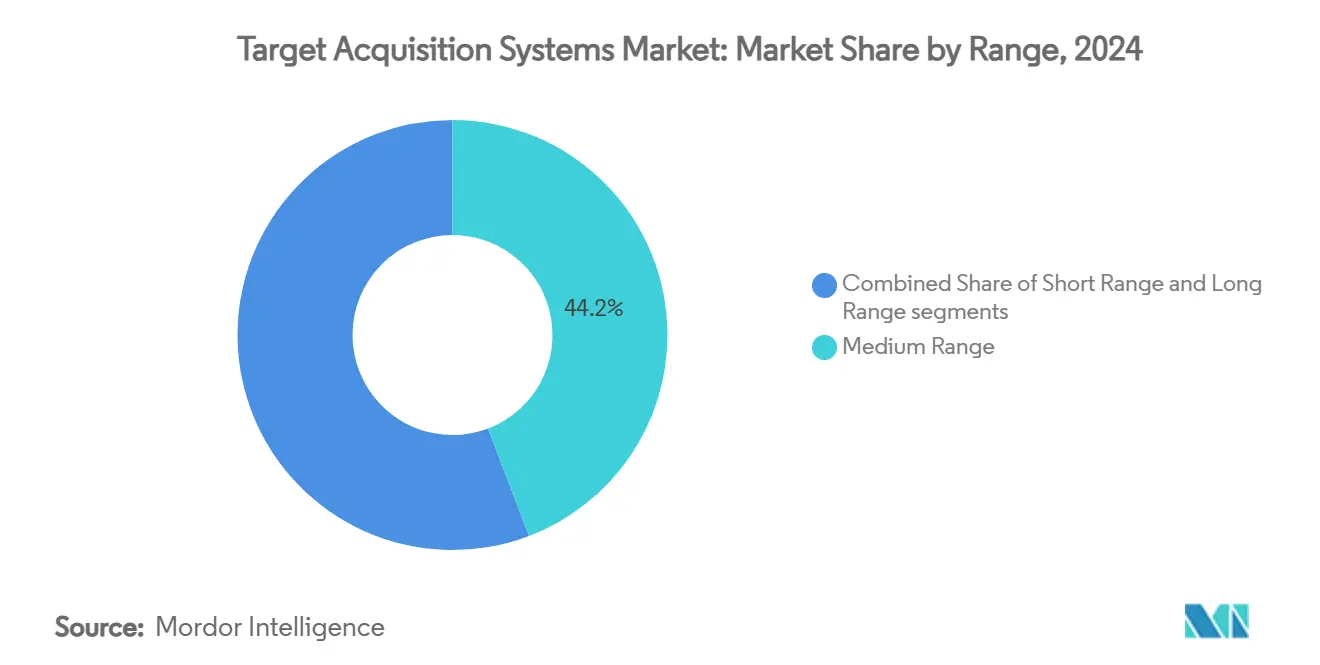

- By range capability, medium-range solutions captured 44.21% of the target acquisition systems market size in 2024, yet long-range systems are forecasted to expand at 7.98% CAGR to 2030.

- By end user, the military segment dominated with 91.20% share of the target acquisition systems market size in 2024, while homeland security demand is advancing at a 6.25% CAGR.

- By geography, North America commanded 34.52% of 2024 revenue, and Asia-Pacific is poised to register a 7.81% CAGR through 2030.

Global Target Acquisition Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Modernization of land forces to support network-centric warfare capabilities | +1.2% | Global, emphasis on NATO and Asia-Pacific | Medium term (2-4 years) |

| Urgent defense requirements for rapid counter-UAS detection and tracking solutions | +0.8% | Middle East, Eastern Europe, Indo-Pacific | Short term (≤ 2 years) |

| Adoption of AI-driven sensor fusion for autonomous threat recognition and cueing | +0.7% | North America, Europe, selected Asia-Pacific | Medium term (2-4 years) |

| Advancements in EO/IR sensor miniaturization enabling dismounted soldier integration | +0.9% | Early adoption in United States, Israel, Europe | Short term (≤ 2 years) |

| Increased dual-use technology funding for ISR payloads through NATO DIANA initiatives | +1.1% | Europe, North America | Long term (≥ 4 years) |

| Rising demand for border surveillance and tactical situational awareness in asymmetric zones | +0.6% | Conflict-prone regions worldwide | Medium term (2-4 years) |

Source: Mordor Intelligence

Modernization of land forces to support network-centric warfare capabilities

Network-centric doctrine now guides every upgrade plan, compelling armed forces to link previously standalone sensors with digital command networks. The US Army’s Autonomous Multi-Domain Launcher demonstrations underline this shift, showing how target acquisition nodes must feed distributed fire-control chains in seconds. European programs mirror the trend: Germany digitizes Puma infantry vehicles with HENSOLDT vision suites so crews can share sensor feeds across battle groups. Retrofit packages are complex because legacy hardware often runs on analog backbones that need secure, low-latency gateways. Operational lessons from recent conflicts confirm that real-time data fusion delivers decisive tactical advantages, accelerating adoption cycles even inside traditionally slow procurement cultures.

Urgent defense requirements for rapid counter-UAS detection and tracking solutions

Commercial drones have exposed gaps in classical air-defense layers, prompting militaries to purchase counter-UAS kits under streamlined contracting rules. Systems such as Teledyne FLIR’s Cerberus XL blend radar, EO/IR, and RF detection to follow quadcopters and fixed-wing UAS at standoff ranges in cluttered airspace.[1]Teledyne FLIR, “Cerberus XL Counter-UAS Platform,” teledyneflir.com The US Army awarded contracts worth over USD 400 million for such solutions in 2024 alone. Algorithms must separate hobby drones from hostile platforms while surviving electronic-warfare noise, which drives heavy investment in AI-based signal classification and sensor fusion. Acoustic arrays and passive RF analyzers increasingly complement radar to cut false-alarm rates in urban terrain.

Adoption of AI-driven sensor fusion for autonomous threat recognition and cueing

Artificial intelligence now underpins the newest generation of targeting electronics. Safran’s Advanced Cognitive Engine uses operational data to boost classification accuracy as environments evolve.[2]Safran, “Advanced Cognitive Engine Unveiled at Eurosatory,” safran-group.com Fusing radar, optical, and acoustic inputs inside edge processors delivers recognition speeds unattainable by single-sensor streams. Yet autonomy introduces cyber and spoofing risks, prompting DARPA’s SABER project to stress-test AI models against adversarial attacks. Program managers, therefore, pair autonomy with human-on-the-loop oversight and spend heavily on curated training data to avoid algorithmic bias.

Advancements in EO/IR sensor miniaturization enabling dismounted soldier integration

Thermal imagers, once confined to vehicles, now fit rifle-mounted housings. Leonardo DRS weapon sights shrink sensors without compromising range or durability, enabling foot soldiers to acquire and designate threats on the move. Gains stem from silicon-photonics wafers, lighter optics, and low-power focal-plane arrays. These hand-held devices mesh with soldier-worn radios so squads can relay target coordinates directly to higher-level shooters. Small-unit lethality rises, as does the complexity of managing permissions for precision fires in congested areas.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged defense procurement timelines and shifting budgetary priorities delay system adoption | −0.9% | Global, most acute in bureaucratic systems | Long term (≥ 4 years) |

| Regulatory challenges in spectrum allocation constrain active radar integration | −0.7% | Varies by national spectrum policy | Medium term (2-4 years) |

| Bottlenecks in sourcing III-V semiconductor focal-plane arrays impact production scalability | −0.5% | Global supply chain, few foundries | Short term (≤ 2 years) |

| Increased vulnerability of digital targeting systems to cyber and electronic-warfare threats | −0.4% | Contested environments worldwide | Medium term (2-4 years) |

Source: Mordor Intelligence

Prolonged defense procurement timelines and shifting budgetary priorities delay system adoption

The US Government Accountability Office notes that even marquee programs like hypersonic weapons lack formal acquisition baselines, complicating industry investment cases. Political turnovers redirect funds mid-cycle, forcing prime contractors to stretch milestones or accept scope cuts. Multinational projects face extra layers of review, since every partner must align export-licensing terms before production can start. When timelines exceed commercial technology refresh rates, systems risk entering service with obsolescent electronics, eroding lifecycle value.

Regulatory challenges in spectrum allocation constrain active radar integration

Military radars compete with 5G, Wi-Fi, and satellite Internet for clean spectrum, especially in the S-band, where propagation suits ground-based and airborne surveillance. The US Department of Defense estimates relocation costs above USD 100 billion should commercial users displace existing allocations. Similar pressures surface worldwide, slowing approvals for new radars and pushing designers toward expensive interference-mitigation hardware. Shared-band operations also raise electromagnetic-compatibility testing overheads during export campaigns.

Segment Analysis

By Platform: Airborne Systems Drive Innovation

Land platforms dominated 40.90% of 2024 revenue, yet airborne assets post the strongest 8.23% CAGR to 2030 as forces seek continuous overwatch across contested zones. Therefore, the target acquisition systems market is transitioning from single-domain emphasis to integrated asset portfolios that pair ground radar with high-altitude imaging. Armored fighting vehicles remain the biggest land sub-segment, propelled by Germany’s Leopard 2 ARC 3.0 retrofit that fuses counter-drone sensors and anti-tank sights.

The USD 13 million United States orders for SMASH 2000L fire-control sights show the rapid uptake of soldier-portable kits that let infantry neutralize micro-drones. On the airborne side, Lockheed Martin’s IRST21 reached Initial Operational Capability on F/A-18s in early 2025, underscoring naval aviation’s appetite for passive long-range detection. Unmanned aircraft also accelerate demand; General Atomics is integrating EagleEye radar into the Gray Eagle 25M, advancing endurance surveillance at the brigade level.

Note: Segment shares of all individual segments available upon report purchase

By Sensor Type: Multi-Sensor Fusion Gains Momentum

EO/IR devices held a 42.17% share in 2024 because they work day or night and resist jamming. Still, fusion suites grow at a 7.26% CAGR as militaries connect radar, optical, laser, and acoustic channels in one processor. That evolution pushes the target acquisition systems market toward software-centric architectures that update via code rather than hardware swaps. GhostEye AESA radar exemplifies radar progress, leveraging gallium-nitride power amps for sharper resolution.

Laser rangefinders remain indispensable; in 2024, Safran won a USD 275 million US Army sustainment contract, ensuring field units can still designate platoon-level precision munitions.[3]GovCon Wire, “Safran Wins USD 275 Million Army Contract for Laser Locators,” govconwire.com HENSOLDT’s CERETRON software platform processes streams from disparate sensors, proving that real-time fusion lifts the probability of correct identification under heavy clutter.

By Range Capability: Long-Range Systems Accelerate

Medium-range products held a 44.21% share in 2024 because most ground engagements unfold within 15 km. Long-range solutions, however, recorded the quickest 7.98% CAGR as anti-access strategies demand standoff strikes. Hypersonic research budgets like the US Navy’s USD 308.3 million contract with Draper for Conventional Prompt Strike guidance amplify calls for seekers able to cue warheads traveling at Mach 5+.

Short-range sensors keep relevance in point defense. India’s USD 3.6 billion Quick Reaction Surface-to-Air Missile buy shows that mobile battalions still need organic sensors to intercept incoming rockets and low-flying drones. The layered defense doctrine blends every range band, creating overlapping pockets of coverage that complicate opponent planning.

Note: Segment shares of all individual segments available upon report purchase

By End User: Homeland Security Applications Expand

Military agencies consumed 91.20% of spending in 2024, but homeland security users will post a 6.25% CAGR as governments harden borders and critical sites. US DHS trials integrate radar, thermal cameras, and unattended ground sensors to monitor remote terrain for illicit crossings. Police forces adopt lightweight counter-drone gear to protect stadium events and energy plants, blurring the military-civil divide and enlarging the target acquisition systems industry's addressable base.

Export-control reviews shape foreign-sales timelines, yet many governments greenlight dual-use EO/IR kits because they resemble commercial security cameras. Firms, therefore, tailor offerings along a continuum: ruggedized, ITAR-free models for civil use and classified variants for frontline troops.

Geography Analysis

North America commands 34.52% of 2024 turnover due to the United States’ unmatched R&D ecosystem and procurement heft. Pentagon programs such as the USD 6.9 billion hypersonic portfolio drive continuous requirements for guidance computers, inertial navigation units, and multi-physics sensor heads. Canada’s focus on Arctic sovereignty leads to sensor packages built to survive snow, ice, and magnetic anomalies, evidenced by Rheinmetall Mission Master CXT testing.[4]Rheinmetall, “Mission Master CXT Trials in Canada’s Arctic,” rheinmetall.com Mexican border surveillance must add small but steady orders, mainly for EO/IR towers and portable acoustic detectors.

Asia-Pacific records the highest trajectory at 7.81% CAGR. China’s USD 314 billion budget overshadows peers, yet the market remains inward-looking. Japan’s 21% uplift to USD 55.3 billion funds interceptor radars and distributed EO nodes for island defense. India advances indigenous design, signing a USD 3.6 billion quick-reaction missile contract and placing follow-on orders for tube-artillery sights valued at USD 850 million. Australia and South Korea collaborate on maritime-patrol sensor kits, opening export lanes to Southeast Asia.

Europe retains a sizeable share rooted in cooperative ventures. The European Sky Shield program pools orders across states to field layered air defenses around shared architectures. Germany’s EUR 200 million (USD 234.43 million) frigate-radar contract underscores cross-border teaming between HENSOLDT and Israel Aerospace Industries. NATO DIANA’s EUR 1.1 billion (USD 1.29 billion) fund accelerates dual-use ISR payloads that can migrate from commercial drones to armored vehicles. Eastern European nations step up buys of counter-UAS radar-optical hybrids in response to nearby conflicts, tightening delivery schedules for suppliers.

Competitive Landscape

The target acquisition systems market shows moderate consolidation. Top defense primes retain the edge by controlling integration know-how, classified supply chains, and sustainment networks. Lockheed Martin Corporation illustrates this strength: its IRST21 achieved operational status on F/A-18s while the company concurrently ran autonomous HIMARS tests and secured USD 857 million in launcher-related awards in 2024. HENSOLDT exploits software-defined CERETRON middleware to ship sensor suites that update via code, cutting life-cycle cost for navies and armies.

White-space entrants attack niches such as neuromorphic chips or quantum-enhanced sensing, promising step-changes once reliability hurdles fall. Collaboration between Raytheon Technologies (RTX Corporation) and Kongsberg Gruppen on GhostEye radar for NASAMS shows incumbents partnering to accelerate AESA roadmaps. Patent filings cluster around AI-based fusion and compressed neural-network weights, indicating that future differentiation may tilt toward algorithms rather than glass and gallium-nitride arrays.

Export-controlled intellectual property remains a competitive lever. Firms that re-package core code in ITAR-free formats gain access to wider audiences. Meanwhile, local offsets and tech-transfer demands, such as India’s K9 Vajra co-production, push primes to share blueprints with national champions or risk exclusion.

Target Acquisition Systems Industry Leaders

-

Lockheed Martin Corporation

-

RTX Corporation

-

Safran SA

-

Leonardo S.p.A

-

Elbit Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Lockheed Martin's Missiles and Fire Control unit secured a USD 1.735 billion contract from the US Department of Defense to produce and maintain the Army's Modernized Target Acquisition Designation Sight/Pilot Night Vision System (M-TADS/PNVS).

- June 2025: RTX Corporation, in collaboration with the Norwegian government and Kongsberg Defence and Aerospace, announced that Norway will participate in developing the GhostEye radar, a mobile medium-range air and missile defense sensor for the National Advanced Surface-to-Air Missile System (NASAMS).

- February 2025: QinetiQ partnered with the US Army to develop the multi-phase prototyping program for the Future Advanced Long-range Common Optical/Netted-fires Sensor (FALCONS) system, replacing the current Long-Range Advanced Scout Surveillance System.

Global Target Acquisition Systems Market Report Scope

Target acquisition systems are used by defense operators to detect and identify targets with enough detail to aid in the effective deployment of lethal and non-lethal means to neutralize a stationary or moving target. The target acquisition systems market is segmented by platform into the land, airborne, and naval platforms. The report also offers the market sizes and forecasts for the target acquisition systems market across the major regions in the world. For each segment, the market sizes and forecasts have been done based on value (USD billion).

| By Platform | Land | Armored Fighting Vehicles (AFVs) | ||

| Soldier Portable/Infantry Systems | ||||

| Artillery and Missile Launcher Integrated | ||||

| Airborne | Fixed-Wing Aircraft | |||

| Rotary-Wing Aircraft | ||||

| Unmanned Aerial Vehicles (UAVs) | ||||

| Naval | Surface Combatants | |||

| Submarines | ||||

| Unmanned Surface/Underwater Vehicles | ||||

| By Sensor Type | Electro-Optical/Infrared (EO/IR) | |||

| Radar | ||||

| Laser Rangefinders and Designators | ||||

| Acoustic and Seismic | ||||

| Multi-Sensor Fusion Suites | ||||

| By Range Capability | Short | |||

| Medium | ||||

| Long | ||||

| By End User | Military | Army | ||

| Air Force | ||||

| Navy | ||||

| Special Operations Forces | ||||

| Homeland Security | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Rest of South America | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Rest of Africa | ||||

| Land | Armored Fighting Vehicles (AFVs) |

| Soldier Portable/Infantry Systems | |

| Artillery and Missile Launcher Integrated | |

| Airborne | Fixed-Wing Aircraft |

| Rotary-Wing Aircraft | |

| Unmanned Aerial Vehicles (UAVs) | |

| Naval | Surface Combatants |

| Submarines | |

| Unmanned Surface/Underwater Vehicles |

| Electro-Optical/Infrared (EO/IR) |

| Radar |

| Laser Rangefinders and Designators |

| Acoustic and Seismic |

| Multi-Sensor Fusion Suites |

| Short |

| Medium |

| Long |

| Military | Army |

| Air Force | |

| Navy | |

| Special Operations Forces | |

| Homeland Security |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the target acquisition systems market?

The market is valued at USD 14.25 billion in 2025 and is projected to reach USD 19.13 billion by 2030 at a 6.07% CAGR.

Which platform segment is expanding fastest?

Airborne systems post the highest 8.23% CAGR through 2030 as forces seek continuous, wide-area surveillance.

Why are multi-sensor fusion suites gaining traction?

They merge radar, EO/IR, laser and other inputs through AI processing, boosting detection accuracy and shrinking false-alarm rates compared with single-sensor setups.

Which region offers the most growth potential?

Asia-Pacific leads with a 7.81% CAGR, fueled by record defense budgets in China, Japan and India.

How are counter-UAS requirements shaping demand?

Layered drone defenses require integrated detection layers, driving rapid procurement of systems such as Teledyne FLIR’s Cerberus XL and related software-defined radars.

Page last updated on: June 30, 2025