Animal Feed Trace Minerals Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

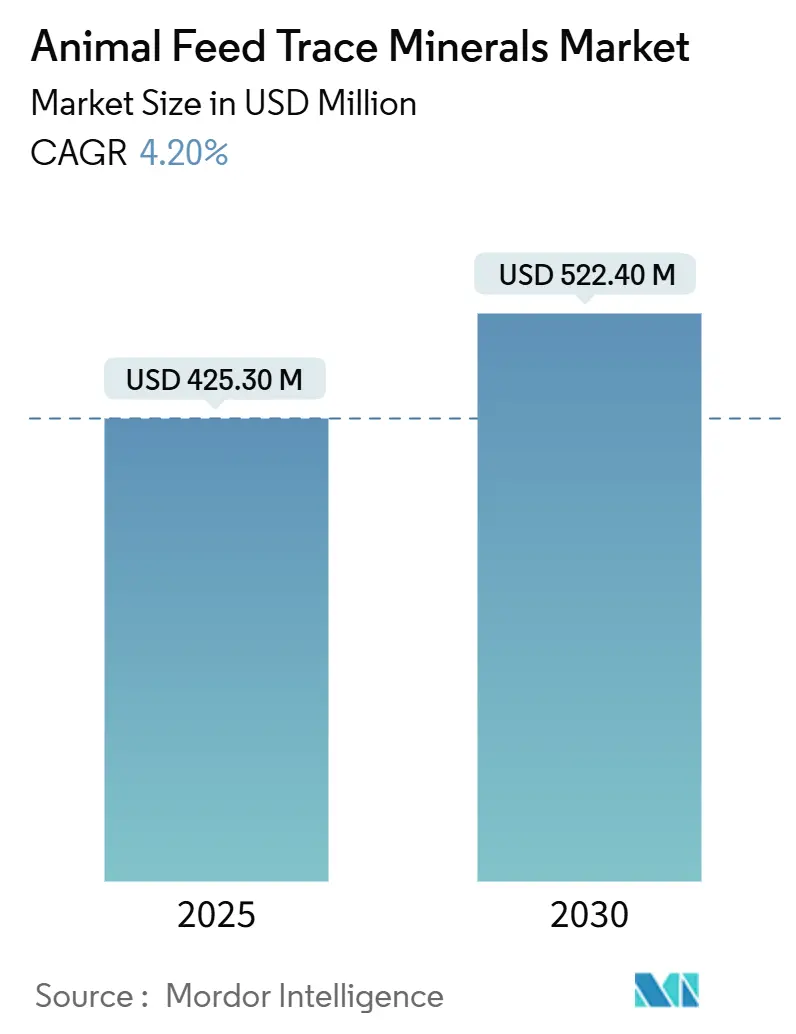

| Market Size (2025) | USD 425.30 Million |

| Market Size (2030) | USD 522.40 Million |

| Growth Rate (2025 - 2030) | 4.20% CAGR |

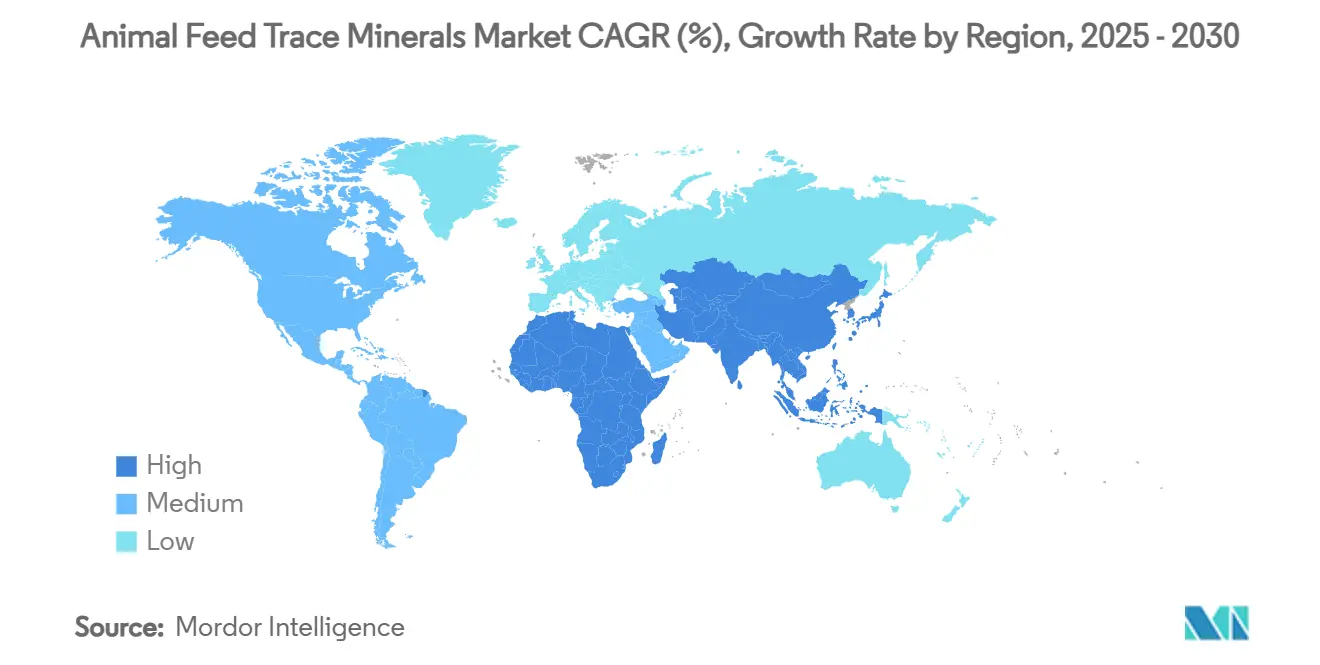

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Animal Feed Trace Minerals Market Analysis by Mordor Intelligence

The feed trace minerals market is valued at USD 425.3 million in 2025 and is projected to reach USD 522.4 million by 2030, growing at a CAGR of 4.20% during the forecast period. The market is shifting from traditional volume-based supplementation to data-driven programs that enhance mineral bioavailability, reduce waste, and meet stricter environmental regulations. The market growth is driven by increasing global demand for animal protein, expanding antibiotic-free production requirements, and improved absorption efficiency of 20-40% through chelation chemistry compared to sulfate salts. The Asia-Pacific region leads market demand, supported by intensive livestock operations and aquaculture expansion that maximize feed conversion benefits. Organic chelates are growing faster than inorganic salts as agricultural operations focus on performance improvements to justify higher formulation costs. Environmental regulations limiting heavy-metal excretion and requiring precise dosing continue to support the premium status of highly bioavailable mineral sources.

Key Report Takeaways

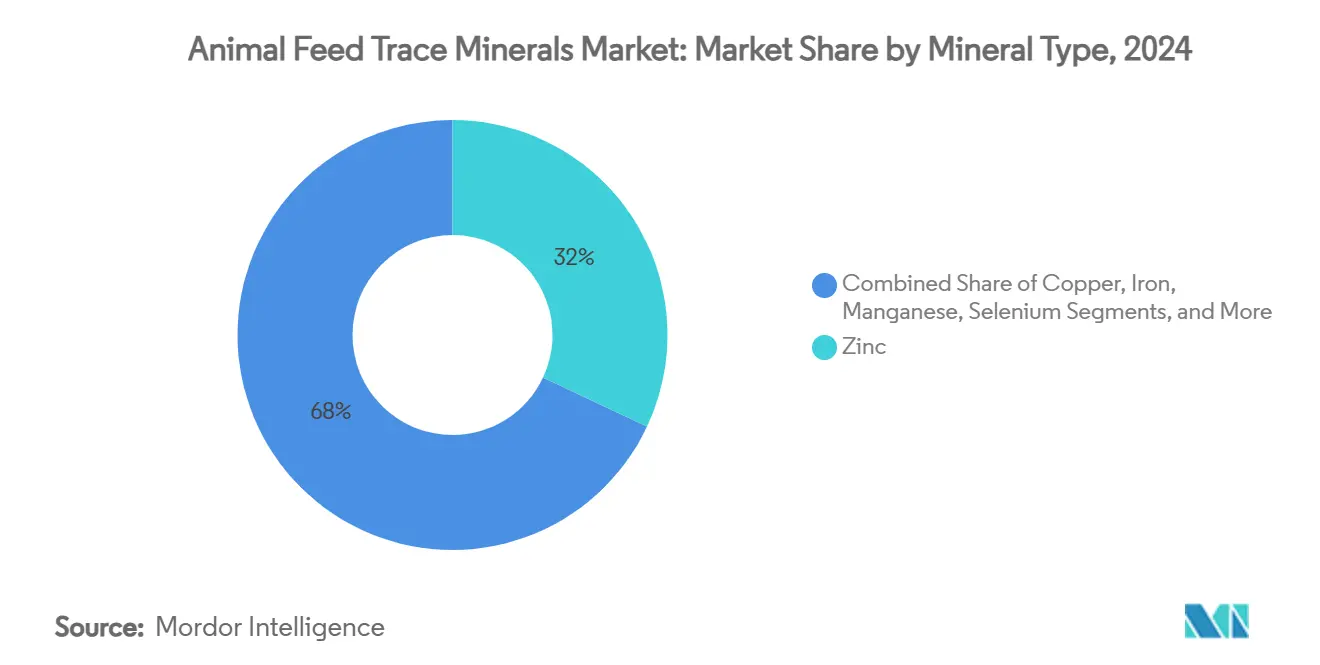

- By mineral type, Zinc dominated with a 32% market share in 2024, while selenium is growing at a 4.9% CAGR through 2030.

- By livestock, poultry contribute 38% of global revenue in 2024, while aquaculture is expanding at a 5.0% CAGR through 2030.

- By source type, inorganic salts represented 65% of the market in 2024, with organic chelates growing at a 5.1% CAGR through 2030.

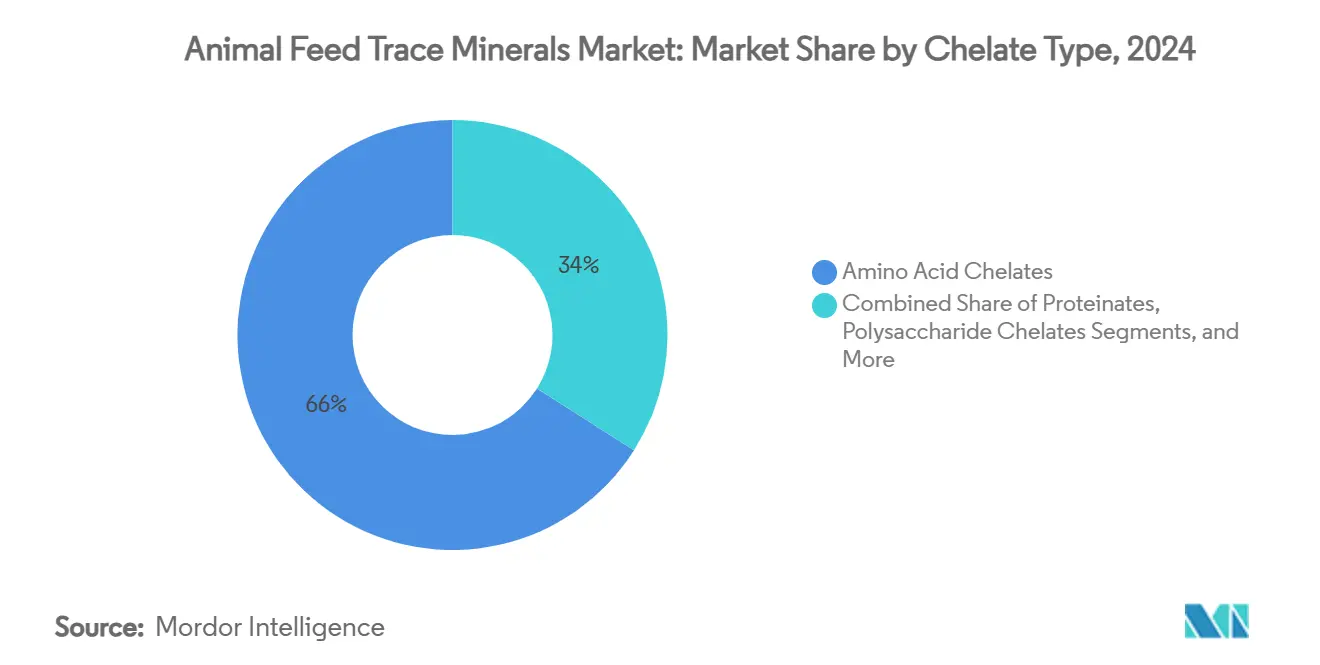

- By chelate types, amino acid chelates held a 66% market share in 2024, with propionates growing at a 5.5% CAGR through 2030.

- By form, dry products accounted for 70% of market share in 2024, while liquid form products are growing at a 4.3% CAGR during 2025-2030.

- By geography, Asia-Pacific held 41% revenue share in 2024 and is projected to grow at a 5.4% CAGR through 2030.

Global Animal Feed Trace Minerals Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Meat and Dairy Demand | +1.2% | Global, Asia-Pacific leading | Long term (≥ 4 years) |

| Shift Toward Highly Bioavailable Organic Trace Minerals | +0.8% | North America and Europe, Asia-Pacific adoption | Medium term (2-4 years) |

| Technological Advances in Chelation and Micro-encapsulation | +0.6% | Global | Medium term (2-4 years) |

| Regulatory Push for Antibiotic-Free, Fortified Feed | +0.7% | Europe and North America | Short term (≤ 2 years) |

| Manure Heavy-Metal Caps Driving Precision Mineral Inclusion | +0.4% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Aquaculture Boom Requiring Species-Specific Mineral Premixes | +0.5% | Asia-Pacific Core | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Global Meat and Dairy Demand

Global protein consumption is increasing by 1.2% annually until 2030, while livestock herds across multiple regions are decreasing due to disease outbreaks and rising costs. Producers are addressing this gap by enhancing feed conversion through optimized mineral programs that improve performance despite stagnant herd numbers.[1]United States Department of Agriculture, “World Agricultural Supply and Demand Estimates, May 2025,” usda.gov In China, a 5% reduction in milk production during late 2024 increased focus on precise mineral delivery systems that reduce waste.[2]Agriculture and Horticulture Development Board, “China Dairy Market Update 2025,” ahdb.org.uk This trend extends to beef and broiler operations globally, driving the feed trace minerals market as operators pursue efficient productivity solutions amid supply fluctuations.

Shift Toward Highly Bioavailable Organic Trace Minerals

Organic chelates demonstrate 20-40% higher absorption rates compared to sulfate forms, resulting in 3-5% improved feed efficiency and 15-25% reduced fecal mineral output in commercial trials. The premium pricing becomes advantageous in regions with strict heavy-metal runoff regulations and for aging animals with reduced digestive capabilities. Large-scale beef trials indicate that organic zinc correlates with enhanced immune response markers, extending its benefits beyond growth performance measures.

Technological Advances in Chelation and Micro-encapsulation

Advanced chelation technology enables mineral release at targeted pH levels in the digestive system, reducing mineral antagonism and improving absorption. Micro-encapsulation protects minerals during feed processing and reduces nutrient loss in aquaculture environments. Experimental nanocarrier systems show potential for decreasing mineral inclusion rates while maintaining nutritional efficacy.

Regulatory Push for Antibiotic-Free, Fortified Feed

Stricter antibiotic regulations in Europe and the United States have led to a shift in health management budgets toward nutritional immunity tools, particularly selenium and zinc fortification. Research indicates that balanced trace mineral programs enhance vaccine effectiveness and decrease illness rates in broilers and piglets, enabling farms to maintain productivity while meeting compliance requirements. The regulatory environment has made fortified feed essential for integrators serving antibiotic-free retail markets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Key Mineral Prices | -0.6% | Global | Short term (≤ 2 years) |

| Stricter Inclusion Limits Over Environmental Runoff | -0.4% | Europe and North America | Medium term (2-4 years) |

| Competing Precision-Nutrition Tech Reducing Dosage Needs | -0.3% | Tech-advanced markets | Long term (≥ 4 years) |

| Specialty Chelator Supply Bottlenecks | -0.2% | Global | Short term (≤ 2 years) |

Source: Mordor Intelligence

Volatility in Key Mineral Prices

Zinc and copper prices fluctuated between 15% and 25% in 2024 due to supply disruptions in major mining regions, affecting feed budgets of smallholders unable to secure long-term contracts.[3]National Security Institute, “Critical Mineral Supply Chain Risks 2024,” nationalsecurity.si.eduImport tariffs on Mexican and Canadian materials implemented in April 2025 created additional cost pressures, potentially delaying transitions from inorganic to organic sources among price-sensitive buyers.

Stricter Inclusion Limits Over Environmental Runoff

Government policies, including Canada's Lake Erie Action Plan, require a 40% reduction in phosphorus levels by 2025.[4]Government of Canada, “Lake Erie Action Plan 2024 Evaluation,” canada.caThis has led regulators to increase monitoring of trace mineral excretion. The resulting guidelines increase the demand for chelated minerals while adding compliance requirements and analytical testing expenses for producers who must verify reduced manure concentrations.

Segment Analysis

By Mineral Type: Zinc Dominance Faces Selenium Challenge

Zinc dominates the feed trace minerals market with a 32% share in 2024, driven by its essential functions in immune system support and reproductive health. Its importance grows as climate-related challenges increase disease risks, particularly in humid environments. Selenium shows the highest growth rate with a projected 4.9% CAGR through 2030, primarily due to its antioxidant properties, crucial in intensive livestock production. These two minerals constitute over 50% of the feed trace minerals market value in 2025, highlighting their fundamental role in animal nutrition.

Copper and iron maintain consistent demand levels due to their vital roles in oxygen transportation and enzymatic functions. Manganese usage increases in broiler feed formulations, as research demonstrates enhanced tibia strength at optimal supplementation levels. Cobalt and iodine fulfill specific nutritional requirements, with particular significance in regions where soil iodine deficiency necessitates feed fortification for dairy cattle.

Note: Segment shares of all individual segments available upon report purchase

By Livestock: Poultry Leadership Challenged by Aquaculture Growth

The poultry segment accounted for 38% of the feed trace minerals market size in 2024. The high stocking densities in poultry operations necessitate trace mineral optimization to maintain egg shell quality and broiler daily weight gain. The aquaculture segment is projected to grow at a 5.0% CAGR through 2030, driven by increasing global fish production and the adoption of species-specific premixes to improve feed conversion efficiency in recirculating aquaculture systems.

The ruminant segment maintains steady demand as balanced mineral ratios support rumen microbes essential for milk production. In the swine segment, producers are adapting early-phase diets with butyrate and organic zinc following the EU ban on high-dose zinc oxide, maintaining mineral demand despite lower inclusion rates. The equine and companion animal segments, though smaller in market share, demonstrate consistent demand for premium chelated products, reflecting pet owners' focus on animal wellness.

By Source Type: Organic Chelates Gain Market Share

Inorganic salts maintain a 65% share of global market value in 2024 due to their low cost, while organic chelates are experiencing 5.1% annual growth during 2025-2030. Research on finishing beef cattle demonstrates that chelated copper and zinc increase serum concentrations while reducing manure excretion by 25%, delivering both performance improvements and environmental benefits.

Manufacturing cost reductions through economies of scale and advanced processing technologies are decreasing the price differential between organic and inorganic options. Feed mills across Asia are establishing local supply agreements for organic premixes, increasing adoption among mid-sized farms that previously relied on standard sulfate minerals.

By Chelate Type: Amino Acid Chelates Lead Innovation

Amino acid chelates accounted for 66% of segment revenue in 2024, due to their superior absorption rates and compatibility across animal species. The chemical structure of these chelates protects minerals from binding agents like phytates, increasing bioavailability in corn-soy feed formulations. Propionates are growing at a 5.5% CAGR, appealing to manufacturers requiring extended product stability in tropical storage conditions. Proteinates serve as a balanced option for producers seeking greater stability than sulfates provide while avoiding the higher costs of amino acid complexes.

Note: Segment shares of all individual segments available upon report purchase

By Form: Liquid Concentrates Gain Traction

Dry premixes dominated the market with a 70% share in 2024, as they are compatible with pellet mills and provide extended shelf life. Liquid concentrates, experiencing a 4.3% annual growth rate, enable accurate dosing in automated dairy and fish feeding systems, ensuring dust control and uniform distribution. Encapsulated liquid zinc blends deliver controlled release in shrimp ponds, minimizing the leaching issues associated with powder formulations.

Geography Analysis

Asia-Pacific accounts for 41% of global revenue in 2024 and maintains a 5.4% CAGR. The transformation of China's dairy industry and the growth in India's broiler production create sustained demand for high-performance chelated minerals that improve feed conversion. The expansion of aquaculture operations across Vietnam and Indonesia drives the need for specialized mineral formulations. Government policies promoting nutrient-efficient feeds support market growth in the region.

North America shows consistent growth due to regulations promoting antibiotic-free meat production and requirements to reduce heavy metal content in manure. The recurring threat of avian influenza has prompted producers to integrate mineral supplementation into their immunity management programs. In Canada, initiatives to reduce Lake Erie nutrient pollution encourage the adoption of precision mineral dosing technologies, expanding beyond conventional sulfate supplements.

Europe maintains its position as a mature market with a focus on innovation, particularly as strict mineral inclusion limits and new tariffs on Russian and Belarusian imports increase reliance on local chelate manufacturers. The region leads in developing micro-encapsulated products that combine minerals and functional additives in single particles, improving feed efficiency. South America, the Middle East, and Africa represent smaller but growing markets as commercial farms expand and implement proven methods to improve productivity.

Competitive Landscape

The feed trace minerals market demonstrates moderate fragmentation, with major players holding significant market shares in 2024, with Alltech (8.1%), Cargill, Inc. (8.0%), ADM (7.0%), and DSM-Firmenich (5.8%). These companies maintain their market positions through proprietary chelation patents, robust research and development initiatives, and integrated raw material sourcing that ensures consistent quality. Regional specialists compete by providing location-specific technical services and customizing premixes according to local ingredient compositions.

Market players focus on vertical integration and geographic expansion strategies. For instance, Barentz's acquisition of China's Fengli Group demonstrates the industry's push into growing Asian markets. Major companies are developing data platforms that integrate mineral supplementation with farm performance analytics, expanding beyond traditional supply functions.

The industry is evolving toward outcome-based business models through value chain partnerships. McDonald's partnership with Syngenta and Lopez Foods provides incentives to beef producers who implement Enogen corn, which improves feed efficiency by 5% and enhances mineral absorption. Research and development efforts include rare earth element processing initiatives in the United States to reduce dependence on Chinese supplies, ensuring stable trace mineral availability for North American premix manufacturing.

Animal Feed Trace Minerals Industry Leaders

-

Cargill, Inc.

-

Alltech

-

Archer Daniels Midland (ADM)

-

DSM-Firmenich

-

Zinpro

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Barentz acquired China’s Fengli Group, enhancing its nutraceutical and animal nutrition reach in Asia.

- June 2025: The Swanson Family of Companies purchased D&D Ingredient Distributors, enlarging feed and pet-food capacities.

- September 2024: Novus International, Inc. and Ginkgo Bioworks formed a partnership to develop feed additives, including trace minerals, for the animal agriculture industry.

- June 2024: Bimeda Inc. introduced BOVitalize in the United States, an oral vitamin and mineral supplement containing trace minerals such as selenium, copper, and zinc for beef and dairy cows, bulls, and ruminating calves.

Global Animal Feed Trace Minerals Market Report Scope

Trace minerals provide the essential nutrients animals need for metabolic functions such as growth and development, immunity, and reproduction. The Animal Feed Trace Minerals Market is segmented by Mineral Type (Zinc, Iron, Manganese, Copper, and Others), Livestock (Ruminants, Poultry, Swine, and Others), Source Type (Organic and Inorganic) and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The report offers market size and forecasts in terms of value in USD for all of the above segments.

| By Mineral Type | Zinc | ||

| Copper | |||

| Iron | |||

| Manganese | |||

| Selenium | |||

| Cobalt | |||

| Iodine | |||

| Others | |||

| By Livestock | Poultry | ||

| Ruminants | |||

| Swine | |||

| Aquaculture | |||

| Pets | |||

| Equine | |||

| Others | |||

| By Source Type | Inorganic | ||

| Organic | |||

| By Chelate Type | Amino Acid Chelates | ||

| Proteinates | |||

| Polysaccharide Chelates | |||

| Propionates | |||

| Others | |||

| By Form | Dry | ||

| Liquid | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East | Saudi Arabia | ||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| Zinc |

| Copper |

| Iron |

| Manganese |

| Selenium |

| Cobalt |

| Iodine |

| Others |

| Poultry |

| Ruminants |

| Swine |

| Aquaculture |

| Pets |

| Equine |

| Others |

| Inorganic |

| Organic |

| Amino Acid Chelates |

| Proteinates |

| Polysaccharide Chelates |

| Propionates |

| Others |

| Dry |

| Liquid |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

Key Questions Answered in the Report

What is the current value of the feed trace minerals market?

The market stands at USD 425.3 million in 2025 and is projected to reach USD 522.4 million by 2030.

Which region leads demand for feed trace minerals?

Asia-Pacific leads with 41% revenue share in 2024, due to intensive livestock and aquaculture sectors.

Why are organic chelates growing faster than inorganic salts?

Organic chelates offer 20-40% higher absorption, lower manure excretion, and better compliance with environmental rules, driving a 5.1% CAGR.

Which livestock segment shows the fastest growth?

Aquaculture is expanding at 5.0% CAGR as species-specific premixes lift feed efficiency in intensive fish and shrimp farms.

How do regulations influence the market?

Stricter antibiotic and heavy-metal runoff rules in North America and Europe push producers to adopt more efficient, bioavailable mineral forms.

Who are the key players in the feed trace minerals market?

Alltech, Zinpro, ADM, DSM-Firmenich, and Cargill, Inc. lead via proprietary chelation technologies and integrated supply chains.

Page last updated on: July 2, 2025