Maritime Security Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

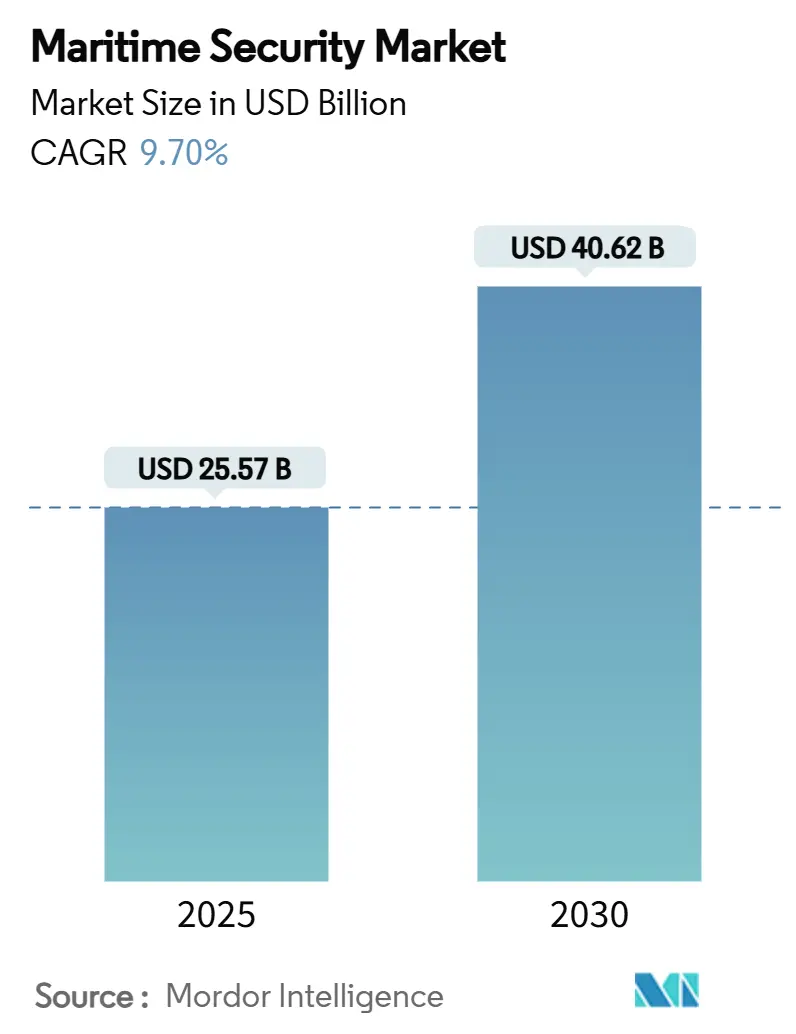

| Market Size (2025) | USD 25.57 Billion |

| Market Size (2030) | USD 40.62 Billion |

| Growth Rate (2025 - 2030) | 9.70% CAGR |

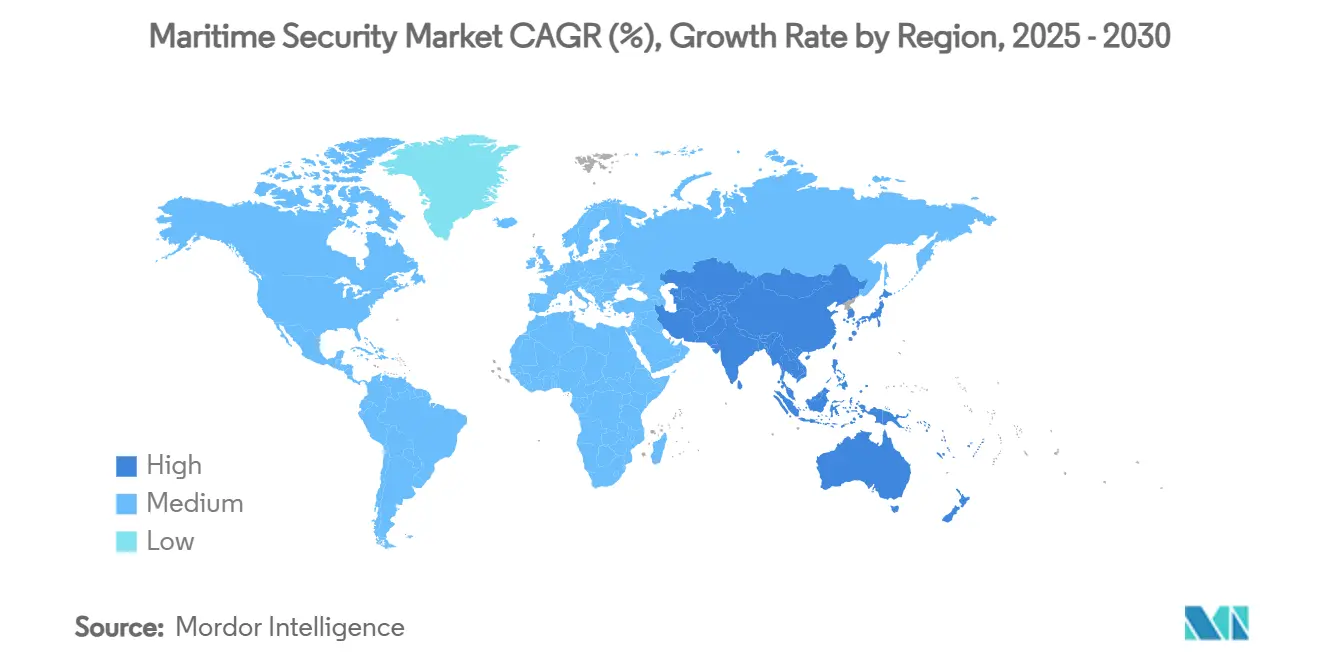

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

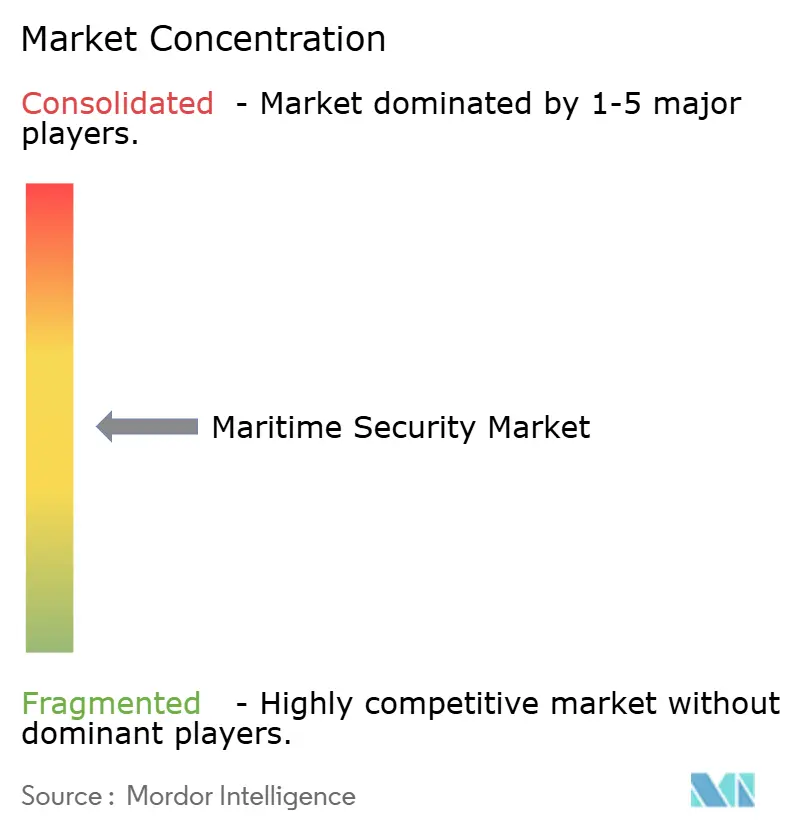

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Maritime Security Market Analysis by Mordor Intelligence

The maritime security market size reached USD 25.57 billion in 2025 and is forecasted to climb to USD 40.62 billion by 2030, advancing at a 9.70% CAGR. Heightened piracy, cyber-enabled sabotage, and expanding regulatory mandates are steering budgets toward integrated surveillance, screening, and resilience platforms.[1]Source: International Maritime Organization, “Dark fleet, decarbonization & geopolitics top maritime focus areas,” imo.org North America retains leadership, supported by rigorous rules and modern port assets, while rapid offshore energy development and multilateral security programmes propel Asia-Pacific’s double-digit growth. Operators are shifting from guard-based deterrence to AI-driven situational awareness, as 69 attacks in the Red Sea alone during November 2023-November 2024 exposed gaps in conventional patrol coverage. Insurance premiums on high-risk routes tripled, strengthening the commercial case for predictive threat-detection suites. Spending now prioritizes interoperable command platforms across ports, vessels, and coastal zones that fuse radar, AIS, video, and cyber analytics.

Key Report Takeaways

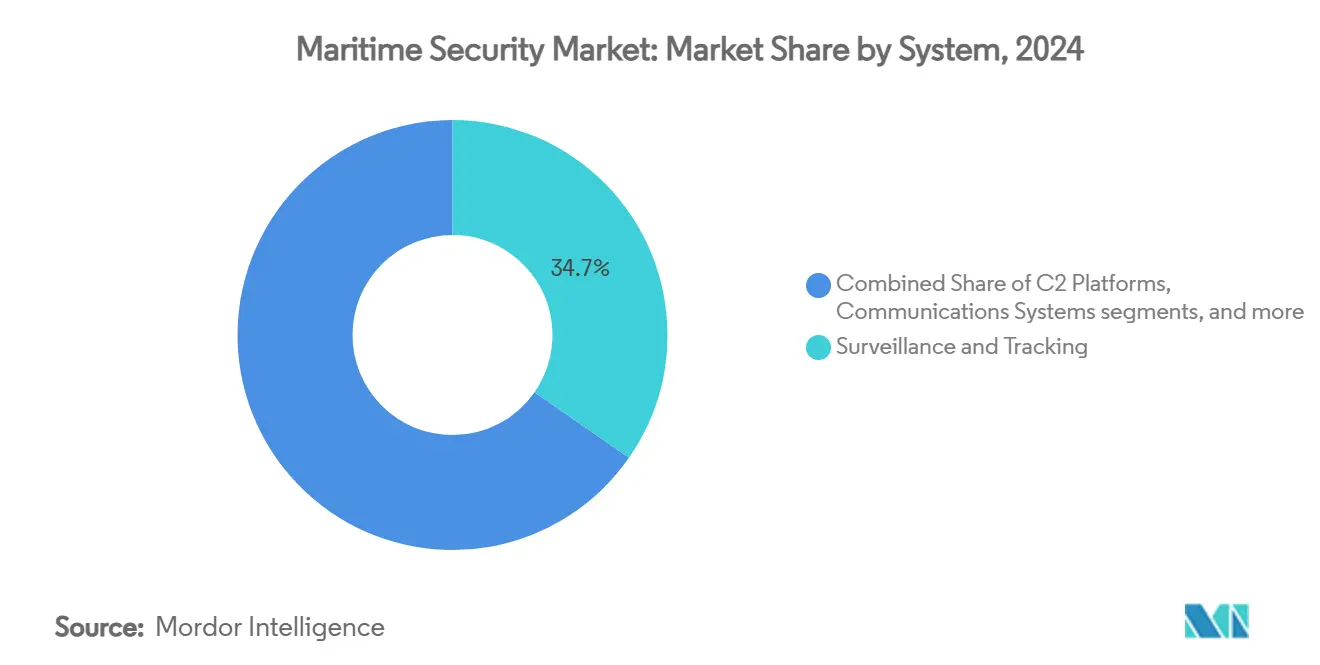

- By system, surveillance and tracking solutions commanded 34.68% of the maritime security market share in 2024, while command-and-control platforms are projected to expand at an 11.45% CAGR through 2030.

- By type, port and critical-infrastructure security held 49.20% revenue in 2024; coastal and border security leads growth at a 10.78% CAGR to 2030.

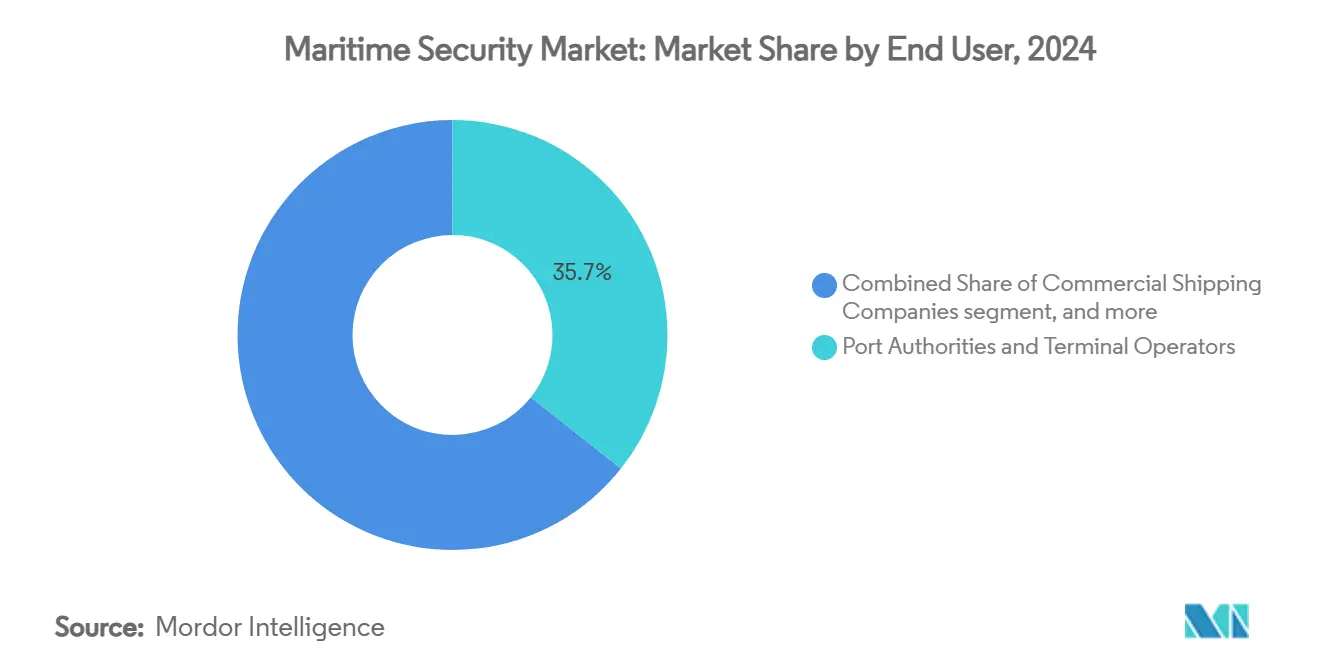

- By end user, port authorities and terminal operators captured 35.67% of demand in 2024; naval and coast guard programs record the fastest CAGR at 10.35% through 2030.

- By geography, North America led with 37.89% revenue in 2024, whereas Asia-Pacific is forecasted to post an 11.20% CAGR to 2030.

Global Maritime Security Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising piracy and maritime threats | +2.1% | Global, especially Red Sea, Gulf of Guinea, SE Asia | Short term (≤ 2 years) |

| Stricter international security regulations | +1.8% | EU, North America, spreading worldwide | Medium term (2-4 years) |

| Growth of global seaborne trade | +1.5% | Asia-Pacific, Middle East key beneficiaries | Long term (≥ 4 years) |

| Adoption of integrated surveillance and screening | +1.4% | Core markets in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Security-linked insurance premium incentives | +0.9% | High-risk shipping corridors | Short term (≤ 2 years) |

| ESG-linked financing drives cyber-resilience | +0.7% | Europe, North America and emerging spill-over | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Piracy and Maritime Threats

The hijackings of MV Ruen (2023) and MV Abdullah (2024) underlined how Somali criminal networks exploited naval redeployments in the Red Sea, reviving ransom-based models. The International Maritime Bureau logged 116 piracy incidents in 2024, and hostage cases tripled to 126 seafarers. This pressured operators to adopt autonomous surface drones monitored by the US Navy’s Task Force 59, which surpassed 50,000 unmanned operating hours. War-risk cover now costs three times pre-crisis levels, incentivising AI-enabled early-warning radars and persistent electro-optic payloads.

Stricter International Security Regulations

The modernised Global Maritime Distress and Safety System (GMDSS) entered force in January 2024, obliging fleets to replace legacy gear with digital communication suites for marine and offshore. [2]Source: Bureau Veritas, “Modernisation of GMDSS enters force 1 January 2024,” marine-offshore.bureauveritas.com In parallel, the US Coast Guard’s July 2025 cybersecurity rule requires every vessel and facility to appoint a Cybersecurity Officer, unlocking a USD 600 million compliance opportunity. Belgium went further, mandating biometric gate control across 40 terminals handling 47,000 identities daily.

Growth of Global Seaborne Trade

UNCTAD projects seaborne volumes to grow 2.4% each year to 2029, raising exposure across higher-value and larger box ships. Container terminals such as Singapore’s Tuas Mega Port deploy driverless vehicles plus AI-powered CCTV to safeguard the world’s biggest automated dock. Industry estimates place global port-security capex at 8-12% of the EUR 2 trillion (USD 2.35 trillion) slated for new berth construction this decade.

Adoption of Integrated Surveillance and Screening

Thales’ CoastShield fuses radar, EO/IR, and AIS feeds to detect surface threats up to 100 nautical miles in adverse weather. Windward’s AI platform now safeguards subsea pipelines after recent sabotage incidents disrupted data-cable routes. OSI Systems secured a USD 32 million order for Eagle M60 mobile scanners as ports accelerate high-energy X-ray adoption.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost and budget constraints | -1.6% | Emerging markets, small operators | Short term (≤ 2 years) |

| Legacy infrastructure integration complexity | -1.2% | Established ports in North America, Europe | Medium term (2-4 years) |

| Data-privacy and sovereignty concerns | -0.8% | Global, with heightened focus in EU, China, Russia | Medium term (2-4 years) |

| Maritime-cyber talent shortage | -0.6% | Global, particularly acute in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

Source: Mordor Intelligence

High Upfront Cost and Budget Constraints

Comprehensive perimeter fencing, biometric gates, and multilayer cargo screening can exceed USD 2 million per terminal, challenging smaller operators whose insurance bills already face 2.5-7.5% increases for 2025 renewals. Global marine insurance premium growth slowed as inflation eroded margins, curbing financing for capital-heavy upgrades.

Legacy Infrastructure Integration Complexity

Switching from Chinese-origin scanners or logistics platforms flagged by US DoT security advisories to NATO-approved equipment involves extended downtime and cybersecurity re-certification. [3]Source: US Department of Transportation, “Worldwide foreign adversarial technological influence advisory,” maritime.dot.gov Initial ISPS Code compliance already cost operators USD 626 million globally, and annual maintenance still absorbs USD 168 million.

Segment Analysis

By System: Surveillance Dominance Drives AI Integration

Surveillance and tracking held 34.68% revenue in 2024, anchoring the maritime security market as operators require continuous domain awareness. Command-and-control (C2) suites are projected to grow 11.45% annually, reflecting the need to orchestrate autonomous surface drones and integrate satellite SAR feeds into a single picture. Saab’s pact with ICEYE underscores how cloud-delivered radar data reshapes tactical decisions. The maritime security market size for surveillance solutions is expected to scale with the broader industry, reaching significant double-digit gains by 2030. Edge analytics embedded in navigation radars allow software patching without hardware swaps, compressing lifecycle costs, and encouraging maritime digital twins for predictive maintenance.

Growing AI capability also elevates screening. OSI Systems’ Eagle M60 contract signalled rising demand for mobile, high-energy drive-through scanners at feeder ports. Modernised GMDSS rules prompt a replacement cycle in maritime radios, driving cross-selling of encrypted data links. Cyber-hardened access systems mandated across Belgian ports validate biometric uptake as a regulatory rather than an optional requirement. As a result, the maritime security market continues to shift from siloed hardware toward modular, software-defined ecosystems, giving prime contractors and niche AI firms parallel growth avenues.

Note: Segment shares of all individual segments available upon report purchase

By Type: Infrastructure Security Leads Coastal Growth

Port and critical-infrastructure solutions delivered 49.20% of 2024 revenue, confirming terminals as the fulcrum of threat-mitigation investment. Coastal and border systems are forecast to grow 10.78% annually through 2030 as states harden exclusive economic zones. The maritime security market size dedicated to coastal surveillance is poised to accelerate as unmanned surface vessels and AI-augmented coastal radars extend coverage beyond 12 nautical miles.

Incumbent port operators use integrated video analytics, radiation portal monitors, and perimeter drones to lower human guard footprints. Belgium’s biometric mandate emphasises how regulation converts best practices into compulsory baselines. Thales’ CoastShield and US Navy unmanned patrols prove the cost-efficiency of autonomous observation over manned patrol craft on coastlines. Vessel security sees steadier momentum because owners weigh retrofits against tripled war-risk premiums, but adoption will rise as insurers reward cyber-certified ships with discounted cover.

By End User: Port Operators Drive Naval Modernization

Port authorities accounted for 35.67% of 2024 spending, highlighting their responsibility to meet ISPS and cyber rules for fixed assets. Modernisation budgets increasingly ring-fence predictive maintenance and digital access control so ports can shorten vessel turnaround while mitigating insider risk. At the same time, naval and coast guard customers should post a 10.35% CAGR to 2030 as governments prioritise maritime domain awareness in defense modernisation. Saab’s order backlog and Thales’ GBP 1.8 billion (USD 2.45 billion) Royal Navy AI maintenance contract underline robust government demand.

Commercial shippers invest tactically, driven by flag-state rules and insurer requirements on high-risk routes. Offshore energy companies adopt subsea-infrastructure monitoring after multiple sabotage episodes, spurring specialist demand for ROV-based surveillance and fibre-optic leak detection. Cruise lines maintain multi-year safety contracts that guarantee periodic kit upgrades, evidencing stable aftermarket revenue streams. The maritime security industry spans regulated civil infrastructure and defense-grade mission needs, intensifying competition among diversified vendors.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America controlled 37.89% of 2024 revenue, underpinned by a mature port estate and stringent security codes. The new US Coast Guard cyber rule generates a USD 600 million compliance niche. At the same time, Lockheed Martin’s AN/TPQ-53 radar demonstrates how open-architecture software upgrades extend land-border devices into littoral monitoring. Canada’s submarine recapitalisation plan and Mexico’s adoption of integrated coastal radars add to continental demand.

Asia-Pacific is the fastest-growing theatre, advancing at an 11.20% CAGR as China scales offshore oil and India funds a USD 125 million domain-awareness project with the US Navy. Japan secured the first DNV cyber certificate for maritime radios prtimes.jp. South Korea unveiled the HCX-23 Plus drone-carrier concept, reflecting heavy naval R&D. These initiatives and Singapore’s rollout of uncrewed harbour patrol boats illustrate state-level commitment to technology adoption.

Europe balances regulatory leadership with pragmatic deployment. The EU added the Red Sea and Gulf of Aden to special areas under MARPOL Annex I, obliging operators to fit additional pollution-control and security gear. Germany and Sweden intensified patrols against shadow-fleet tankers, while Belgium’s biometric rollout sets a continental benchmark. Red Sea turbulence produced 19 pirate incidents in the Middle East and Africa in 2024, prompting Somaliland’s Berbera Port upgrade as an alternative haven, meforum.org. Regional risk profiles determine whether operators favour hard-kill naval options or scalable surveillance grids, but every region converges on AI-enabled situational awareness as the core enabler.

Competitive Landscape

Competition is moderate: established defense primes coexist with fast-growing data analytics specialists. Saab targets 18% organic CAGR through 2027, underpinned by SEK 31.5 billion (USD 3.28 billion) 2023 orders and fresh naval radar projects. Thales leverages multi-year Royal Navy contracts to refine predictive-maintenance algorithms, later repackaged for commercial fleets. Leonardo, Lockheed Martin, and Babcock compete on end-to-end integration and life-cycle support.

Digital entrants scale quickly. FTV Capital’s USD 271 million grab of Windward shows investor appetite for AI that predicts vessel-behaviour anomalies. DNV’s purchase of CyberOwl signals classification societies’ push into continuous cyber monitoring.. Armed with fresh funding and the ‘Marauder’ drone boat, Saronic competes for autonomous-patrol budgets long held by conventional shipbuilders.

Price pressure and integration risk encourage consolidation as buyers prefer single-vendor suites over piecemeal tools. Vendors that bridge physical, digital, and regulatory layers secure durable margins. The maritime security market will, therefore, continue to reward firms able to converge hardware sensors, AI analytics, and compliance management within unified platforms.

Maritime Security Industry Leaders

-

Thales Group

-

BAE Systems plc

-

Saab AB

-

OSI Maritime Systems

-

Smiths Detection Group Limited (Smiths Group plc)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: In partnership with Naval Group, Thales was awarded a contract to develop and supply an advanced sonar suite for the Royal Netherlands Navy's Orka-class submarines under the RNSC (Replacement Netherlands Submarine Capability) program. This system enhances the detection of stealthy underwater threats. Thales, a leader in underwater systems, equips over 50 submarines globally, including SSBNs1 and SSNs2.

- February 2024: The UK Ministry of Defense awarded Thales a contract to strengthen the country's national security. Valued at USD 2.3 billion, this 15-year agreement will enable the Thales Maritime Sensor Enhancement Team (MSET) project to introduce a new era for the Royal Navy. This project aims to optimize ship availability and resilience by harnessing advanced AI and data management tools.

Global Maritime Security Market Report Scope

Maritime security concerns the protection of vessels, ports, and other infrastructure related to the shipping business from intentional damage caused by terrorism, sabotage, or subversion.

The maritime security market is segmented by system, type, and geography. By system, the market is segmented into screening and scanning, communications, surveillance and tracking, and other systems. The other systems include command and control systems, gate or port access control systems, and cybersecurity systems. By type, the market is classified into port and critical infrastructure security, vessel security, and coastal security. The report also covers the sizes and forecasts for the maritime security market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| By System | Screening and Scanning | |||

| Communications Systems | ||||

| Surveillance and Tracking | ||||

| Access Control and Biometrics | ||||

| Command and Control (C2) Platforms | ||||

| Navigation Management and AIS | ||||

| By Type | Port and Critical Infrastructure Security | |||

| Vessel Security | ||||

| Coastal and Border Security | ||||

| By End User | Commercial Shipping Companies | |||

| Port Authorities and Terminal Operators | ||||

| Naval and Coast Guard | ||||

| Oil and Gas Offshore Operators | ||||

| Cruise and Ferry Lines | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Australia | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Rest of South America | ||||

| Middle East and Africa | Middle East | United Arab Emirates | ||

| Saudi Arabia | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Rest of Africa | ||||

| Screening and Scanning |

| Communications Systems |

| Surveillance and Tracking |

| Access Control and Biometrics |

| Command and Control (C2) Platforms |

| Navigation Management and AIS |

| Port and Critical Infrastructure Security |

| Vessel Security |

| Coastal and Border Security |

| Commercial Shipping Companies |

| Port Authorities and Terminal Operators |

| Naval and Coast Guard |

| Oil and Gas Offshore Operators |

| Cruise and Ferry Lines |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the maritime security market?

The maritime security market size stood at USD 25.57 billion in 2025 and is projected to reach USD 40.62 billion by 2030.

Which region leads the maritime security market?

North America led in 2024 with 37.89% revenue share, primarily due to stringent cybersecurity rules and extensive port infrastructure.

Which segment is expanding fastest within the maritime security market?

Command-and-control platforms are forecast to post the quickest growth at 11.45% CAGR, driven by autonomous-vessel integration demands.

Why is Asia-Pacific expected to grow rapidly?

The region benefits from rising offshore energy activities, large-scale domain-awareness programmes such as India’s USD 125 million project, and increased defence modernisation spending.

How are new regulations influencing maritime security investments?

Updated IMO communication rules and the US Coast Guard cybersecurity mandate compel operators to replace legacy systems, generating a USD 600 million compliance opportunity and accelerating adoption of integrated, cyber-resilient platforms.

What technologies are redefining maritime security strategies?

AI-enhanced coastal radars, autonomous surface and underwater drones, high-energy mobile X-ray scanners, and biometric port-access controls are reshaping how operators detect and deter physical and cyber threats.

Page last updated on: July 3, 2025