Municipal Water Treatment Chemicals Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 11.85 Billion |

| Market Size (2030) | USD 15.37 Billion |

| Growth Rate (2025 - 2030) | 5.34% CAGR |

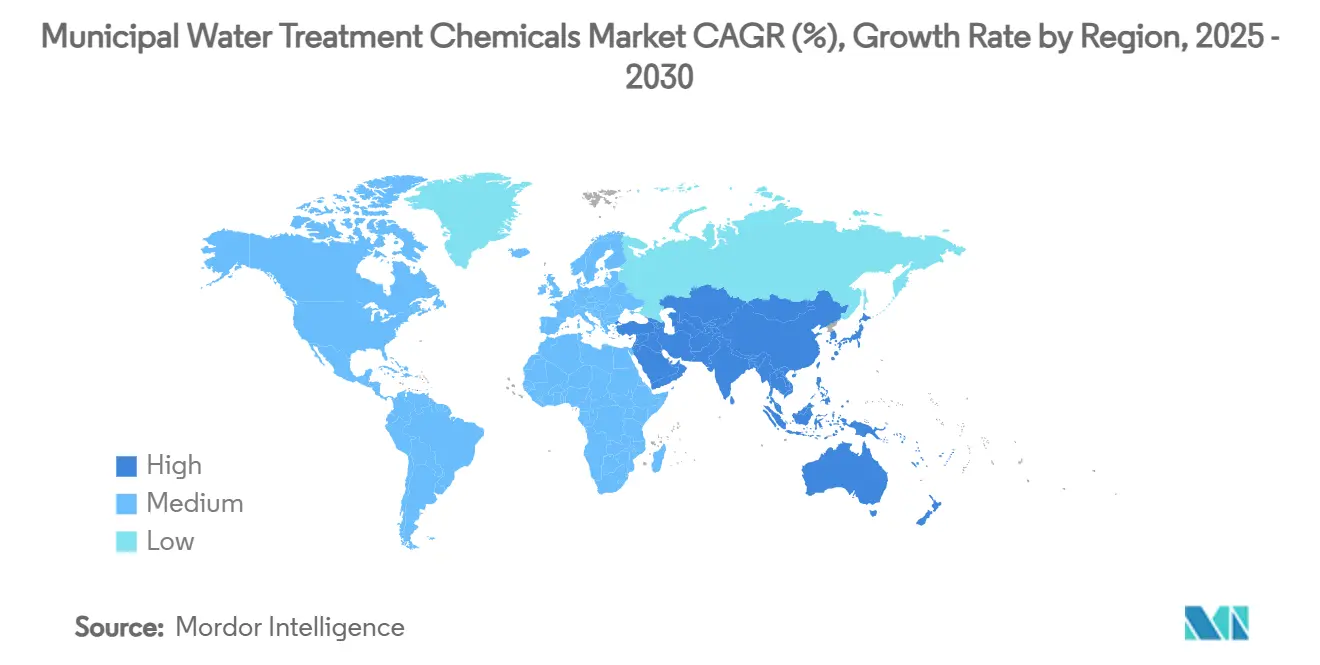

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

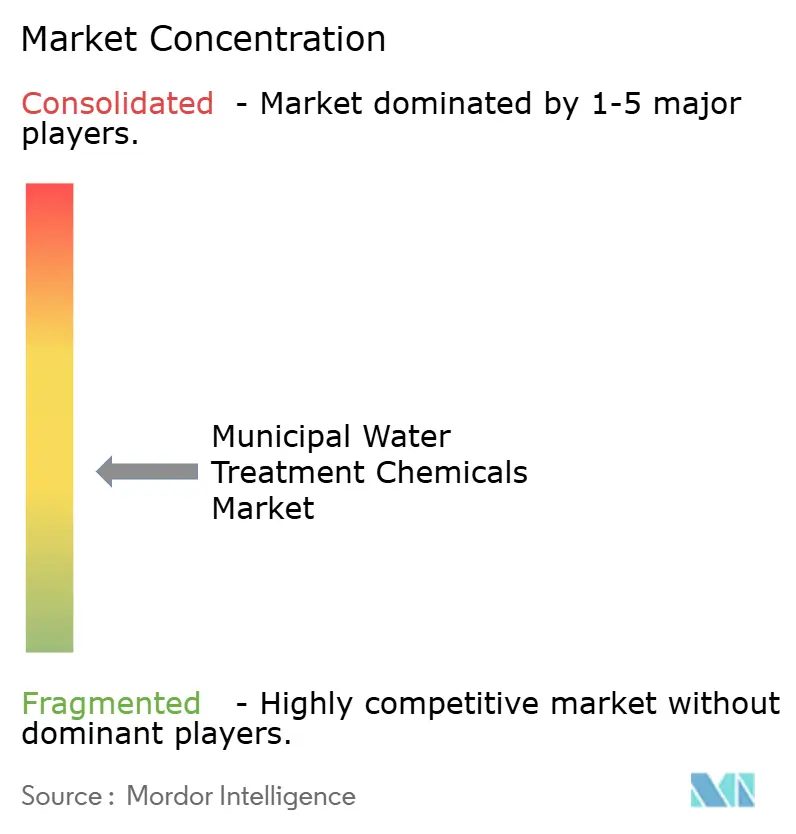

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Municipal Water Treatment Chemicals Market Analysis by Mordor Intelligence

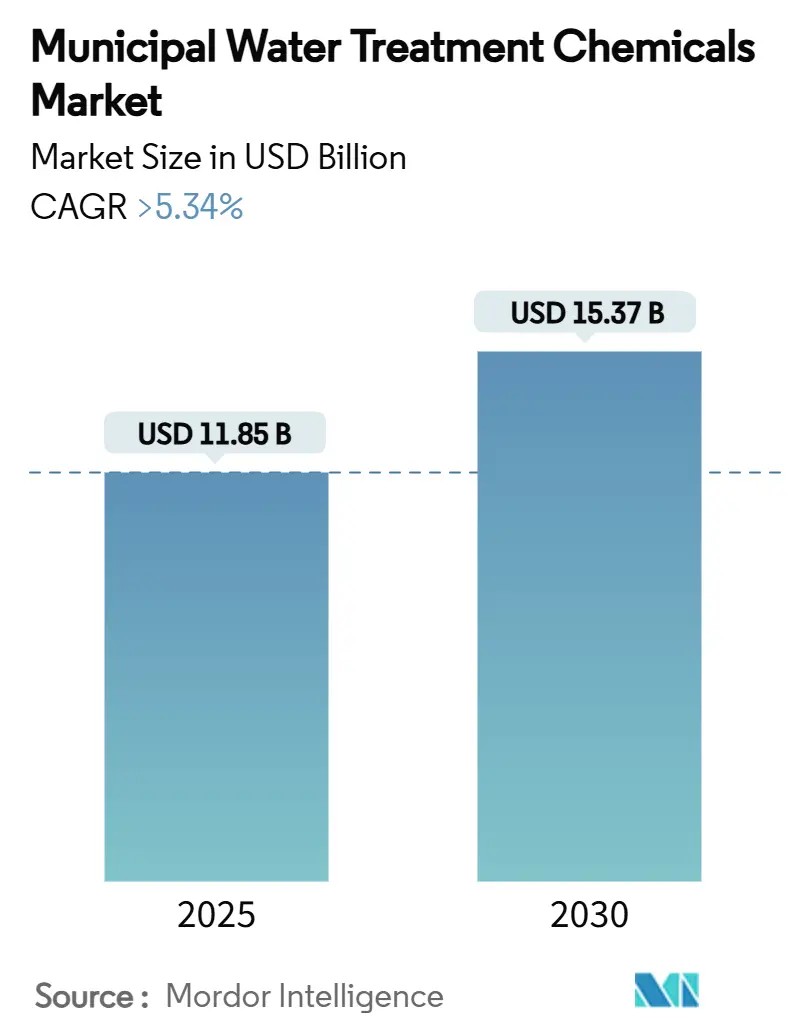

The Municipal Water Treatment Chemicals Market size is estimated at USD 11.85 billion in 2025, and is expected to reach USD 15.37 billion by 2030, at a CAGR of greater than 5.34% during the forecast period (2025-2030). Urbanization, stricter PFAS limits of 4 ppt for PFOA and PFOS, and rising volumes of industrial and municipal wastewater are the pivotal forces shaping demand. Utilities are overhauling plants to comply with the new U.S. EPA rule, adding advanced coagulation, flocculation, and oxidation steps that favour specialized reagents. Coast-line water scarcity is pushing desalination build-outs, while government programmes such as India’s Jal Jeevan Mission accelerate chemistry uptake in high-growth economies. Competitive strategies now combine vertical integration in chlor-alkali, bio-based innovation in flocculants, and digital dosing platforms, giving suppliers new avenues for margin protection and service differentiation.

Key Report Takeaways

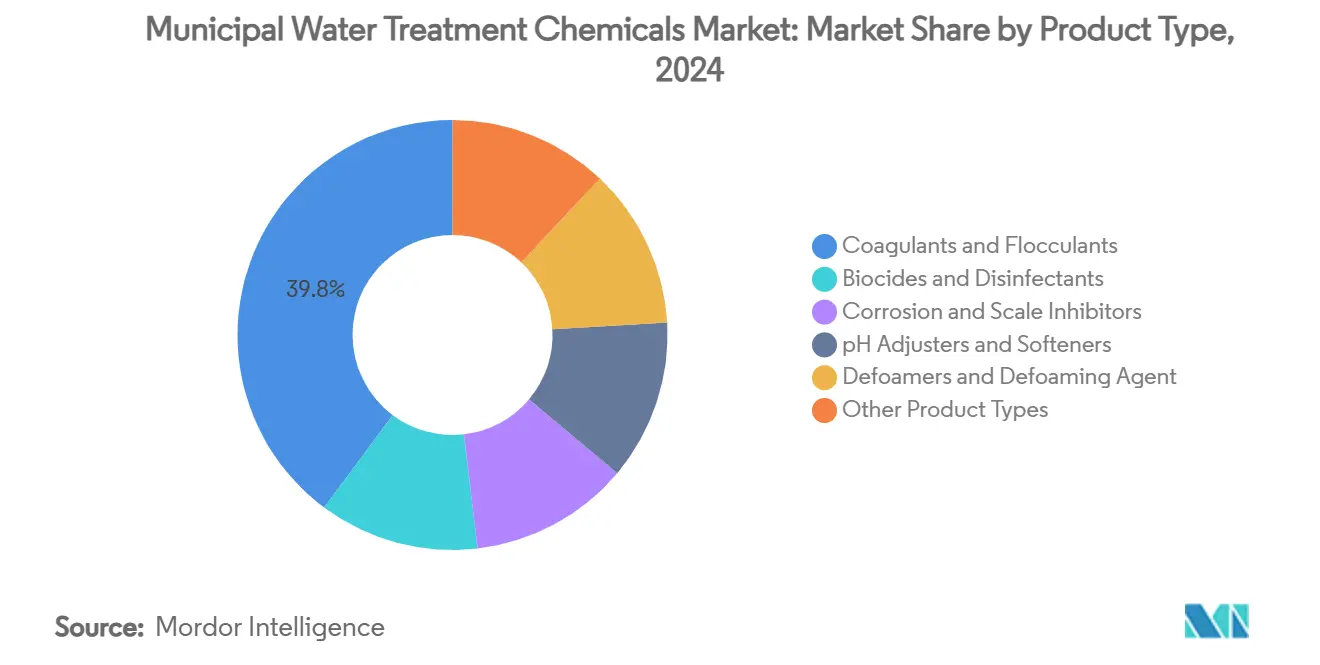

- By product type, coagulants and flocculants held 39.82% of municipal water treatment chemicals market share in 2024; flocculants are set to grow fastest at 7.18% CAGR through 2030.

- By chemistry, inorganic agents commanded 68.36% share of the municipal water treatment chemicals market in 2024; bio-based chemistry is advancing at a 7.45% CAGR over the outlook period.

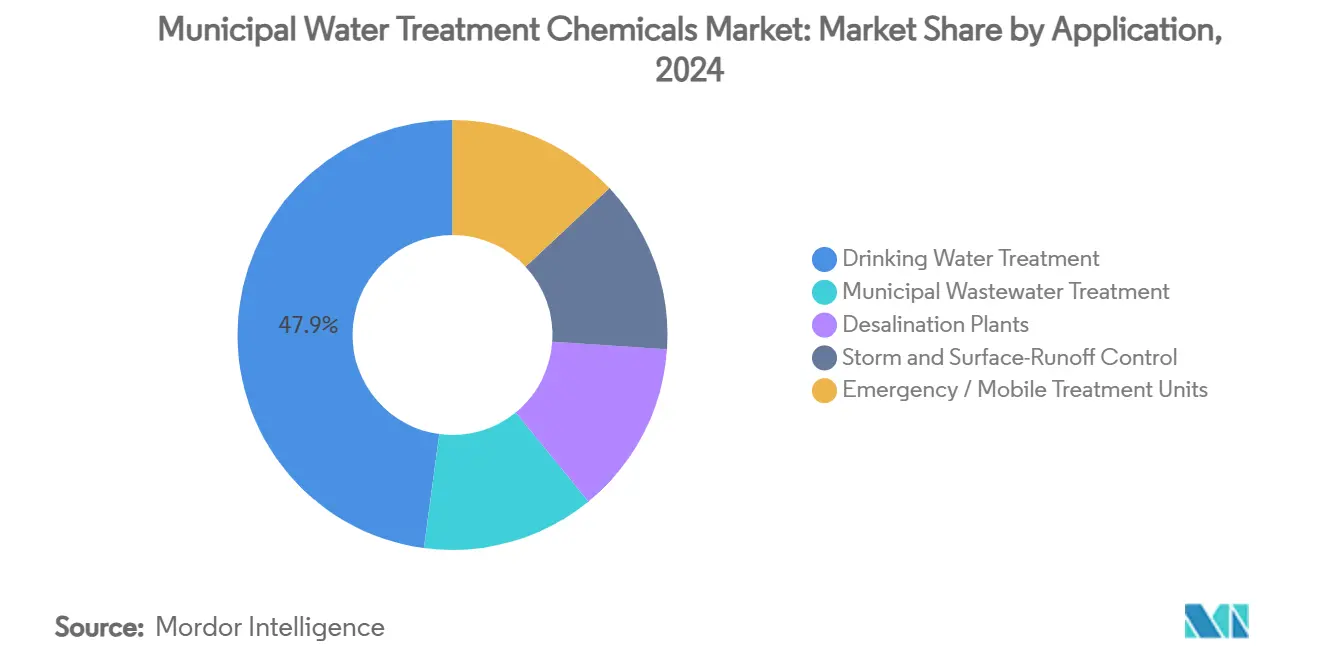

- By application, drinking water treatment led with a 47.88% share of the municipal water treatment chemicals market size in 2024, while desalination plants are forecast to expand at 6.92% CAGR to 2030.

- By geography, Asia-Pacific captured 33.19% revenue share in 2024; the region is projected to post the highest 7.61% CAGR through 2030.

Global Municipal Water Treatment Chemicals Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban population growth and aging distribution networks | +1.2% | Global, with highest impact in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Tightening discharge norms for PFAS/micropollutants | +0.8% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Industrial expansion raising wastewater volumes | +0.9% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Water-reuse mandates raising demand for advanced treatment chemicals | +0.7% | Global, led by water-scarce regions | Long term (≥ 4 years) |

| Decentralized containerised plants needing precise chemical dosing | +0.6% | Global, particularly rural and remote areas | Short term (≤ 2 years) |

Source: Mordor Intelligence

Urban Population Growth and Aging Distribution Networks

Global urban dwellers are increasing at 1.84% annually, straining legacy pipes that corrode and scale, thereby elevating consumption of phosphate-based corrosion inhibitors[1]. The United States Infrastructure Investment and Jobs Act earmarked billions for pipe rehabilitation, yet only 25% has been deployed, leaving a significant backlog that will lift medium-term chemical purchases. Higher density wastewater now contains more complex particulate loads, prompting utilities to double-dose polyaluminum chloride and ferric chloride to meet turbidity limits. Lime-soda ash softening remains prevalent for hardness trims from 35-40 grains down to near 5 grains, but environmental objections to brine discharge are steering cities toward alternative sequestrants.

Tightening Discharge Norms for PFAS/Micropollutants

The 2024 EPA final rule obliges 4,100-6,700 systems to meet PFAS MCLs, with compliance costs pegged at USD 1.5 billion per year. Utilities are rapidly trialling cationic surfactants such as CTAC in concert with alum to reach >80% PFAS removal, while peracetic-acid advanced oxidation shows promise against trace pharmaceuticals. Regulatory deadlines of April 2027 for monitoring and April 2029 for full compliance compress adoption windows and favour turnkey chemical solutions over capital-intense membranes.

Industrial Expansion Raising Wastewater Volumes

Forecasts place the wider water and wastewater treatment sector above USD 1 trillion by 2033, a function of surging industrial output. Semiconductor fabs demand ultrapure water and generate high-alkaline effluents, while Asia-Pacific textile plants produce dye-laden discharges of 200-600 mg/L BOD and heavy metals that necessitate Fe-Al composite coagulants achieving 90% phosphorus removal. Pharmaceutical effluents rich in antibiotics drive uptake of advanced oxidation and specialty biocides capable of degrading recalcitrant organics.

Water-Reuse Mandates Raising Demand for Advanced Treatment Chemicals

California targets 800,000 acre-feet of recycled water by 2030, doubling to 1.8 million by 2040, stimulating orders for high-grade coagulants, membrane aids, and UV‐AOP dosing packages. Singapore’s NEWater, Brazil’s Aquapolo, and new onsite reuse ordinances in Austin and Miami highlight the global pivot toward quaternary treatment trains that require finely tuned chemistry for particle destabilization and pathogen control.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward physical and membrane-based treatment alternatives | -0.4% | Global, led by developed markets | Medium term (2-4 years) |

| Feedstock price volatility for chlor-alkali and petrochemical inputs | -0.3% | Global, with highest impact in regions dependent on imports | Short term (≤ 2 years) |

| Public push-back on chlorination and chemical additives | -0.2% | North America and EU, expanding to urban centers globally | Long term (≥ 4 years) |

Source: Mordor Intelligence

Shift Toward Physical and Membrane-Based Treatment Alternatives

Reverse osmosis and thin-film nanocomposite membranes now provide robust contaminant rejection without heavy chemical pretreatment, reducing coagulant demand by up to 40% in some plants. AI-enabled membrane bioreactors further trim chemical doses by 75%, though fouling risks and periodic chemical cleaning temper full displacement potential.

Feedstock Price Volatility for Chlor-Alkali and Petrochemical Inputs

Electricity-intense chlor-alkali faces volatile power tariffs as grids pivot to intermittent renewables, lifting unit costs for sodium hypochlorite, ferric chloride, and caustic soda. Polymer flocculants suffer similar swings when naphtha-derived monomers spike, prompting producers to lock long-term energy and ethylene contracts or backward-integrate into brine electrolysis.

Segment Analysis

By Product Type: Coagulants Drive Market Leadership

Coagulants and flocculants held a commanding 39.82% revenue share in 2024 within the municipal water treatment chemicals market. Metal salts such as polyaluminum chloride remain indispensable for destabilizing colloids, whereas bio-flocculants like chitosan-based LaChiPur are gaining traction at a rapid 7.18% CAGR thanks to biodegradability advantages. Sodium hypochlorite volumes continue to climb, yet UV-chlorine hybrids are nibbling at traditional disinfectant growth. Pipe corrosion-control agents post steady gains as utilities tackle aging networks. Multifunctional blends that combine coagulation, scale inhibition, and residual control illustrate the industry’s move toward chemistry packs that cut operator complexity and drum inventories.

Flocculant innovation spans cationic polyacrylamide copolymers for microplastics capture and tannin-based powders that lower sludge production by 15-20%. Demand for pH adjusters remains tied to lime-soda softening in hard-water markets, even as zero-liquid-discharge mandates drive alternative softness-achieving chemistries. Silicone-based defoamers centred around polymethylsiloxanes occupy a specialised but vital niche in high-shear aeration basins, preventing foam-borne bacterial plume carryover that undermines clarifier performance.

Note: Segment shares of all individual segments available upon report purchase

By Chemistry: Inorganic Chemicals Dominate Despite Bio-Based Innovation

Inorganic reagents controlled 68.36% of 2024 sales in the municipal water treatment chemicals market, anchored by aluminium sulphate, ferric chloride, and chlorine derivatives. Economies of scale, proven efficacy, and wide raw-water compatibility underpin their dominance. Yet bio-based chemistry, while just 5% today, expands at 7.45% CAGR. Natural extracts from Moringa oleifera seeds, crab-shell chitosan, and lignin derivatives are penetrating sludge-cost-sensitive utilities seeking metal-free residues. Kemira’s claim that 47% of its input stream already comes from renewable or recycled materials exemplifies incumbent pivot.

Synthetic organics still play a key adjunct role, especially cationic and anionic polyacrylamides that bridge particles after primary coagulation. Next-generation polyDADMAC variants show superior charge-neutralization in low-alkalinity waters, reducing metal dosages by 10–15%. Research into alginate-clay composites blends inorganic backbones with renewable binders, promising hybrid performance at competitive cost, further blurring classical chemistry lines.

By Application: Drinking Water Treatment Leads Growth

Drinking water treatment held a 47.88% revenue share in 2024 across the municipal water treatment chemicals market and remains the primary compliance driver under the new PFAS rule. Coagulant dosages in some U.S. plants have risen 25% post-rule to reach 60–70 mg/L as operators push removal efficiency ahead of 2027 monitoring deadlines. Wastewater treatment remains the second-largest outlet, coping with higher industrial COD and nutrient loads that demand specialty agents like Fe-Al blends for simultaneous phosphorus capture.

Desalination is the fastest climber, forecast at 6.92% CAGR to 2030 as Algeria, Saudi Arabia, and a string of Indian coastal states expand reverse-osmosis capacity[2].Frontiers in Membrane Science and Technology, “Desalination Market Outlook,” frontiersin.org Pretreatment antiscalants and biocides must now conform to tighter discharge regulations, fuelling uptake of biodegradable phosphonate-free formulations. Climate-driven storm-water surges and emergency-response deployments reinforce demand for portable dosing skids, an area where Ecolab and Veolia market containerised treatment trains pre-loaded with multi-action reagent cartridges.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific dominates with a 33.19% share of 2024 global revenue and exhibits the fastest 7.61% CAGR through 2030. India alone eyes USD 2.8 billion market value by 2025 as Jal Jeevan Mission races toward universal piped water. Chinese textile and semiconductor clusters discharge high-COD and dye-laden streams; over 80% of industrial effluent historically entered watercourses untreated, bringing a wave of chemical retrofits. Concurrent desalination megaprojects in China and Australia demand low-fouling antiscalants and bio-compatible co-agents that extend membrane life.

North America, while mature, is pivoting to compliance-driven replacement cycles. The municipal water treatment chemicals market in the region is buoyed by the EPA PFAS rule with USD 1.5 billion annual recurring chemical spend. U.S. infrastructure grants prioritise lead-service-line replacements, a move that enlarges phosphate corrosion inhibitor volumes. Canadian utilities are shifting from gas-chlorination to onsite hypochlorite generation, trimming transport hazards and favouring more concentrated brines.

Europe maintains long-standing environmental directives such as the Water Framework Directive, sustaining robust demand for premium coagulants that meet low aluminium residue limits. AMP 8 in the United Kingdom will unlock fresh tenders favouring suppliers that offer circular-economy credentials and sludge-reduction chemistries. Nordic utilities integrate renewable energy, including biogas cogeneration in digestion, boosting sales of chemical aids that stabilise anaerobic processes. EU legislation encouraging water reuse is spawning quaternary treatment packages, and suppliers of specialty oxidants and coagulant synergists are capitalising.

Competitive Landscape

Global leadership remains moderately fragmented. Ecolab’s USD 50 million acquisition of Barclay Water Management added proprietary monochloramine technology that reduces Legionella risk and expands a northeastern U.S. service base. Solenis is scaling polyvinylamine capacity via a USD 193 million Virginia plant that shortens supply chains for U.S. utilities.

Digitalisation has moved centre-stage: DuPont’s WAVE PRO software simulates ultrafiltration scenarios, cutting over-design safety factors and enabling lower chemical overfeeds. SNF continues global polyacrylamide expansions, integrating upstream acrylamide monomer plants to shield against naphtha swings. Veolia’s Delaware PFAS plant showcases bundled EPC plus chemical supply, proving the appeal of solution sales over pure commodity delivery. Private equity activity, such as H.I.G. Capital’s purchase of USALCO, underscores the cash-flow resilience of regulated water markets and accelerates consolidation.

Start-ups focusing on bio-flocculants, peracetic-acid oxidation catalysts, and AI-enhanced dosing are emerging, but scale-up hurdles and customer qualification cycles favour incumbents with established supply networks. Still, regulatory tailwinds for greener chemistries open white-space niches that agile innovators can seize, especially in regions where sludge-disposal costs equal 20–25% of OPEX.

Municipal Water Treatment Chemicals Industry Leaders

-

Ecolab (Nalco Water)

-

Kemira

-

BASF SE

-

Solenis

-

Veolia Water Technologies & Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Veolia inaugurated a USD 35 million PFAS removal plant in Delaware to treat water for 100,000 residents using granulated activated carbon. This adds to advancements in municipal water treatment chemicals, improving drinking water safety.

- November 2024: Ecolab has completed a USD 50 million acquisition of Barclay Water Management. This adds the proprietary iChlor® monochloramine system to its municipal water treatment chemicals portfolio for treating Legionella bacteria.

Global Municipal Water Treatment Chemicals Market Report Scope

The municipal water treatment chemicals market report includes:

| By Product Type | Biocides and Disinfectants | ||

| Coagulants and Flocculants | |||

| Corrosion and Scale Inhibitors | |||

| pH Adjusters and Softeners | |||

| Defoamers and Defoaming Agent | |||

| Other Product Types | |||

| By Chemistry | Inorganic | ||

| Organic | |||

| Bio-based | |||

| By Application | Drinking Water Treatment | ||

| Municipal Wastewater Treatment | |||

| Desalination Plants | |||

| Storm and Surface-Runoff Control | |||

| Emergency / Mobile Treatment Units | |||

| By Geography | Asia-Pacific | China | |

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| NORDIC Countries | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

| Biocides and Disinfectants |

| Coagulants and Flocculants |

| Corrosion and Scale Inhibitors |

| pH Adjusters and Softeners |

| Defoamers and Defoaming Agent |

| Other Product Types |

| Inorganic |

| Organic |

| Bio-based |

| Drinking Water Treatment |

| Municipal Wastewater Treatment |

| Desalination Plants |

| Storm and Surface-Runoff Control |

| Emergency / Mobile Treatment Units |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

Key Questions Answered in the Report

What is the current Municipal Water Treatment Chemicals Market size?

The municipal water treatment chemicals market size reached USD 11.85 billion in 2025 and is forecast to grow to USD 15.37 billion by 2030.

Which segment is expanding the fastest?

Flocculants are projected to register the highest 7.18% CAGR through 2030 as utilities adopt bio-based polymers for better biodegradability.

How will PFAS regulations influence chemical demand?

The 2024 U.S. EPA PFAS rule compels 4,100-6,700 systems to install new treatment processes, underpinning an additional USD 1.5 billion in annual chemical spending.

Why is Asia-Pacific leading market growth?

Rapid urbanization, large-scale industrial discharge, and government-backed water infrastructure programmes give Asia-Pacific a 7.61% CAGR edge through 2030.

What role do bio-based chemicals play in the industry?

Bio-based coagulants and flocculants, though a small share today, are growing at 7.45% CAGR because they lower sludge volume and align with tightening sustainability standards.

Page last updated on: July 15, 2025