Market Overview

| Study Period | 2019 - 2030 |

| Market Volume (2025) | 3.78 Million tons |

| Market Volume (2030) | 4.56 Million tons |

| Growth Rate (2025 - 2030) | 4.90% CAGR |

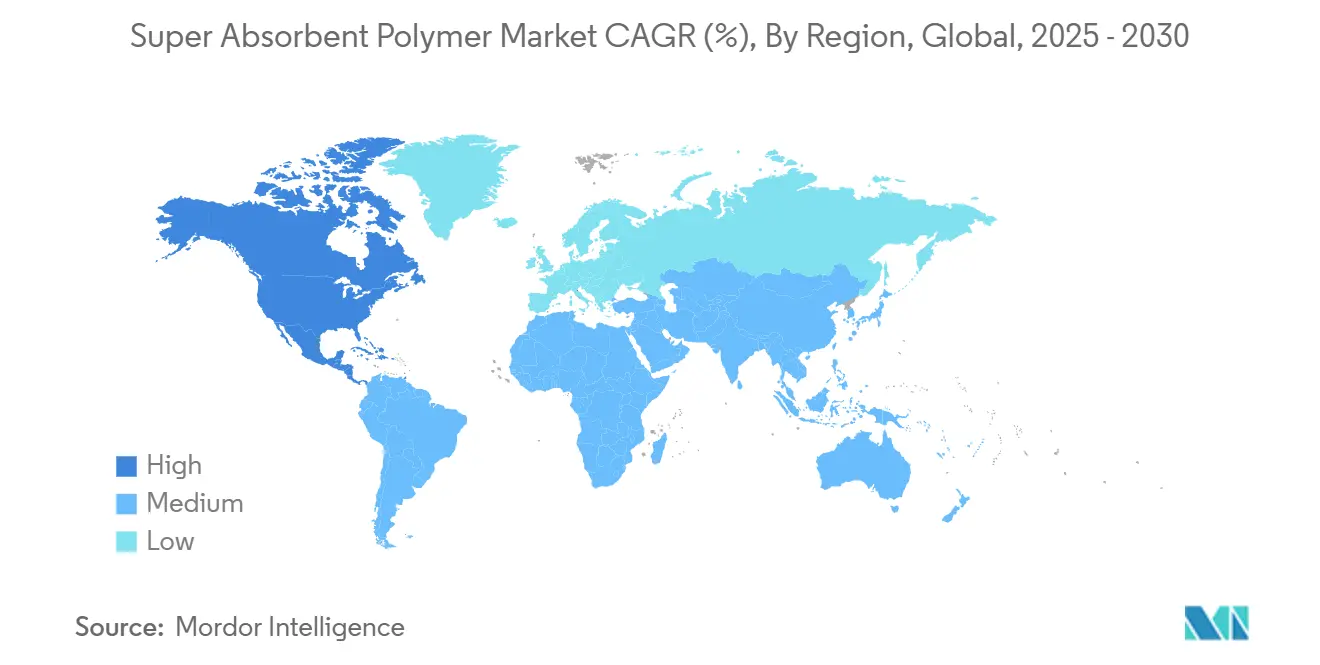

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Super Absorbent Polymers (SAP) Market Analysis by Mordor Intelligence

The super absorbent polymers (SAP) market stands at 3.78 million tons in 2025 and is forecast to reach 4.56 million tons by 2030, reflecting a 4.9% CAGR during 2025-2030. Enlarging demand in baby diapers, rapid uptake of high-SAP adult incontinence pads, and a widening set of industrial and agricultural applications are the core forces behind this steady expansion. Tightening European regulations that reward bio-based chemistries, together with higher per-capita diaper spend in China and India, are reshaping product portfolios toward premium, high-performance grades. Manufacturers continue to upgrade plants for energy efficiency and vertical integration to buffer acrylic acid price swings. At the same time, direct-to-consumer subscription models and e-commerce-driven cold-chain packaging unlock high-margin niches that compensate for margin pressure in standard hygiene volumes. Rising investment in cellulosic and starch-derived alternatives signals that sustainability now drives both brand value and process innovation in the super absorbent polymers market.

Key Report Takeaways

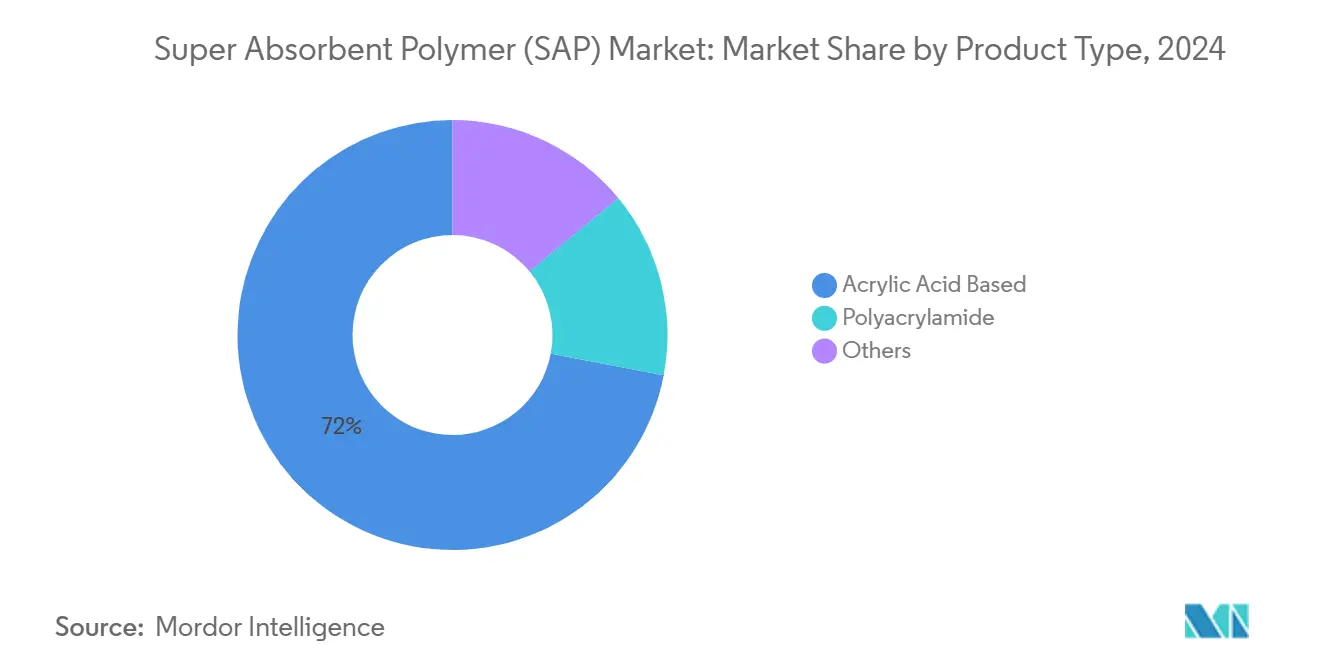

- By product type, acrylic-acid SAPs led with 72% of the super absorbent polymers market share in 2024, while polyacrylamide variants are advancing at a 6.6% CAGR through 2030.

- By polymerization process, gel polymerization captured 60% revenue share in 2024; solution polymerization is forecast to grow at 5% CAGR through 2030.

- By application, baby diapers accounted for 65% of the super absorbent polymers market size in 2024; adult incontinence is projected to expand at a 5.37% CAGR between 2025-2030.

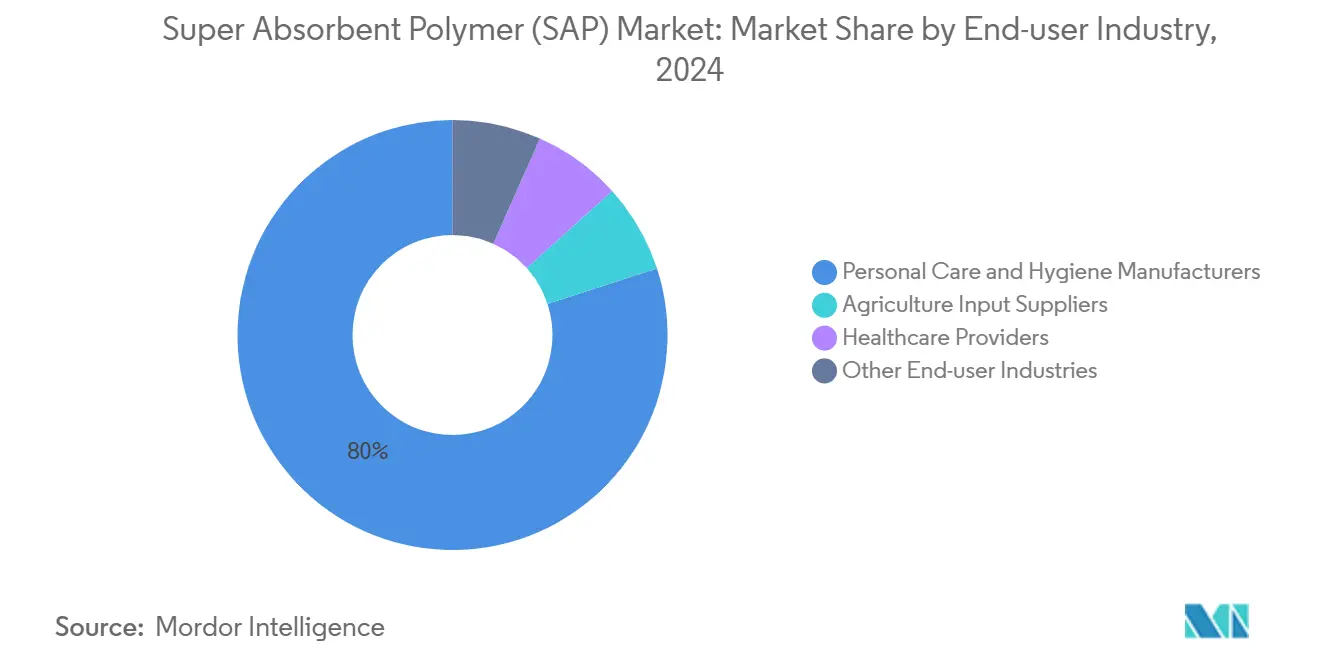

- By end-user industry, personal care manufacturers held 80% revenue share of the super absorbent polymers market in 2024, whereas agricultural input suppliers show the fastest 6% CAGR outlook.

- By geography, Asia-Pacific commanded 42% of the super absorbent polymers market in 2024; North America records the quickest 5.50% CAGR for 2025-2030.

Global Super Absorbent Polymers (SAP) Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising per-capita diaper spend in China and India | +1.2% | Asia-Pacific (China, India) | Medium term (2-4 years) |

| Rapid adoption of high-SAP adult incontinence pads | +0.9% | Japan, South Korea, Western Europe | Medium term (2-4 years) |

| Shift to bio-based SAP in the EU | +0.6% | Europe; spillover to North America | Long term (≥ 4 years) |

| E-commerce-led demand for absorbent packaging | +0.4% | Developed markets worldwide | Short term (≤ 2 years) |

| Expanding agricultural applications | +0.5% | Water-stressed farming regions | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Per-Capita Diaper Spend in China and India

Urban households in China lifted their average diaper outlay by 15% since 2022, aided by policy changes that support larger families and rising disposable income. In India, distribution build-out in tier-2 and tier-3 cities raised penetration, bringing advanced diaper formats within reach of first-time buyers. Premium SKUs contain higher-capacity SAP grades and reduced gel blocking, accelerating unit consumption and value growth across the super absorbent polymers market. Local converters increasingly lock supply via long-term offtake deals to secure quality and mitigate freight risks.

Rapid Adoption of High-SAP Adult Incontinence Pads

Demographic aging in Japan, South Korea, Germany, and Italy has elevated adult incontinence prevalence, while social acceptance campaigns reduce stigma. New pads integrate up to 40% more SAP, enabling thinner profiles that resemble regular underwear and encourage daytime use. Subscription e-commerce channels are growing, bundling discrete delivery, leakage guarantees, and mobility-specific SKUs. Producers respond with differentiated core-shell particle morphologies that boost absorption under load, creating a high-margin sub-segment within the super absorbent polymers market.

Shift to Bio-Based SAP in EU Driven by Packaging Rules

The EU Packaging and Packaging Waste Regulation, effective February 2025, mandates recyclability and sets minimum recycled content targets, indirectly steering end-users toward cellulosic or starch-rich SAP chemistries. Leading suppliers launched cellulose-based grades that retain 80% of the absorption capacity of petrochemical SAPs yet biodegrade within one year. Purdue University’s hemp-derived hydrogel demonstrates 250-300 g/g uptake while breaking down in under six months, offering a promising route for premium hygiene and controlled-release agricultural products[1]Purdue University, “Purdue researchers develop sustainable, biodegradable superabsorbent materials from hemp,” purdue.edu. Higher margins, consumer trust, and compliance advantages sustain capital inflows toward this green niche of the super absorbent polymers market.

Expanding Agricultural Applications

Field trials prove that SAP-amended soils cut irrigation by 15-30% and raise drought-season yields up to 15%[2]Utah State University Extension, “Commercially Available Products to Increase Soil Water-Holding Capacity for Gardens and Landscapes,” usu.edu . Polyacrylamide-based SAPs excel due to controlled water release and compatibility with urea coatings. Chinese policy incentives for water conservation accelerate adoption in arid northern provinces, boosting local output and intensifying competition for export orders.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw material prices | −0.8% | Global; non-integrated producers hit hardest | Short term (≤ 2 years) |

| Safety concerns over residual monomers | −0.4% | Premium markets worldwide | Medium term (2-4 years) |

| High production cost | −0.2% | Small-scale producers in all regions | Medium term (2-4 years) |

Source: Mordor Intelligence

Volatile Raw Material Prices

Acrylic acid constitutes up to 70% of production cost, and quarterly swings as wide as 25% destabilize procurement budgets. Changhong Polymer’s USD 1.6 billion propane-to-acrylic-acid plant, due in 2026, could lower variable cost curves and unsettle pricing parity among established Western suppliers. Interest in bio-routes and vertical integration rises as boards prioritize feedstock security.

Safety Concerns Over Residual Monomers

Studies detecting trace PFAS, VOCs, and unreacted acrylates in diapers have heightened scrutiny, especially in the European Union, Japan, and coastal China. Market leaders now apply extra purification to cut residual monomer to below 10 ppm, trimming regulatory risk but adding 3-5% to unit cost and pressuring price-sensitive segments of the super absorbent polymers market.

Segment Analysis

By Product Type: Acrylic Dominates While Polyacrylamide Accelerates

The acrylic fraction represented 72% of the super absorbent polymers market share in 2024, anchored by its proven reliability in baby diapers. To bolster safety perception, premium brands specify higher-purity acrylic SAPs with lower free monomer levels. In parallel, polyacrylamide grades are expanding at a 6.6% CAGR, propelled by their superior water retention in arid agriculture and industrial sealing. Within the super absorbent polymers market size context, polyacrylamide volumes are forecast to add 125 kilotons between 2025 and 2030, capturing incremental share from acrylic grades.

Product developers pursue hybrid networks that mix acrylic and polysaccharide backbones to marry cost and degradability. Nippon Shokubai’s biomass-derived SAP line, certified Halal and produced in Indonesia, exemplifies such cross-chemistry innovation. Investment emphasis now tilts toward biomass sourcing logistics, impurity control, and scalable continuous reactor designs that ensure consistent polymer architecture.

Note: Segment shares of all individual segments available upon report purchase

By Polymerization Process: Gel Technology Leads Manufacturing Methods

Gel polymerization kept a 60% revenue share in 2024, with its reactor trains optimized for high throughput and uniform cross-link density. Energy recovery loops and continuous monomer recycling drive incremental cost competitiveness. Solution polymerization grows at 5% CAGR because it enables small-lot, specialty grades with tight molecular weight distribution and reduced energy load, aligning with sustainability targets.

Suspension and inverse-suspension routes persist in niche roles that require unique particle morphologies, such as core-shell microspheres for medical fluid management. Process engineers focus on precise cross-linker feed control and in-line spectroscopy to tune absorption under load, further segmenting supply within the super absorbent polymers market.

By Application: Baby Diapers Lead While Adult Incontinence Surges

Baby diapers consumed 65% of the super absorbent polymers market size in 2024, underpinned by steady birth numbers in South Asia and premiumization in the United States and Western Europe. Thinner, stretch-waistband designs employing dual-core SAP distribution enable leakage reduction and permit higher retail pricing. The mature diaper segment, therefore, remains a stable profit engine even as volume growth normalizes.

Adult incontinence represents the fastest-expanding application, with a 5.37% CAGR projected through 2030. Subscription models, discrete packaging, and gender-specific fits unlock new consumer cohorts. Producers engineer particle size distributions that raise absorption under pressure, ensuring comfort for ambulatory users. Feminine hygiene and medical wound care add niche demand; absorbent packaging and cable-blocking gels round out smaller yet lucrative verticals within the super absorbent polymers market.

By End-User Industry: Personal Care Dominates While Agriculture Grows Fastest

Personal care and hygiene multinationals secured 80% of global demand in 2024, emphasizing long-term supply contracts, rigorous quality audits, and joint research and development agreements. Their scale supports continuous line upgrades that boost efficiency and cut waste. Meanwhile, agriculture input suppliers post the highest 6% CAGR, catalyzed by drip-irrigation installers and micro-fertigation integrators. Controlled-release SAPs that incorporate micronutrients let farmers address water scarcity and soil fertility with a single product, lifting total addressable value.

Healthcare providers procure SAP-based dressings for chronic wound exudate management, valuing sterilization stability and low cytotoxicity. Specialties such as telecom cable fillers and refrigeration gel packs comprise the “other industries” bracket, proving that tailored performance parameters unlock recurring, defensible revenue slices across the super absorbent polymers market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific held 42% of the super absorbent polymers market in 2024, powered by China’s integrated acrylic acid-SAP clusters that minimize feedstock logistics. Government incentives, notably in Jiangsu and Shandong, support capacity debottlenecking and export-oriented expansions. India contributes volume growth through broader diaper penetration, while Japan retains a technology leadership niche in specialty and biomass-derived grades.

North America is projected to post the fastest 5.50% CAGR through 2030. Growth arises from premium diaper SKUs, high-SAP adult incontinence adoption among aging baby boomers, and specialized industrial uses such as fracking water blockers and cold-chain pads. Research consortia with land-grant universities pioneer cellulosic and protein-based networks, aligning corporate sustainability pledges with regulatory trends. The region also records early field use of hemp-based SAP in horticulture, reinforcing circular economy narratives within the superabsorbent polymers market.

Europe’s stringent policy climate accelerates bio-based uptake and packaging recyclability. Germany leads production volume, whereas Nordic countries drive consumer preference for compostable diaper cores. Compliance costs spur alliances between polymer suppliers and waste-management firms to pilot closed-loop recovery schemes. EU standards increasingly influence export formulations, compelling global producers to harmonize product safety and labeling.

Competitive Landscape

The market is highly consolidated. Chinese challengers expand aggressively, leveraging captive acrylic acid, economies of scale, and domestic logistical synergies. Differentiation shifts toward specialty chemistries, cradle-to-grave sustainability credentials, and application-specific technical service. Western producers answer via open-innovation programs with start-ups that supply enzymatic or catalytic breakthroughs for bio-monomer production, aiming to hold margin in the evolving super absorbent polymers market.

Super Absorbent Polymers (SAP) Industry Leaders

-

NIPPON SHOKUBAI CO., LTD.

-

BASF

-

SUMITOMO SEIKA CHEMICALS CO.,LTD.

-

LG Chem

-

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2024: BASF completed a USD 19.2 million upgrade at its Freeport, Texas super absorbent polymers plant, raising throughput and energy efficiency.

- August 2024: NIPPON SHOKUBAI CO., LTD., announced a 50,000 ton per year SAP expansion in Indonesia, scheduled to start operations in July 2027.

Global Super Absorbent Polymers (SAP) Market Report Scope

The scope of the Super Absorbent Polymers (SAP) market report includes:

| By Product Type | Polyacrylamide | ||

| Acrylic Acid Based | |||

| Others | |||

| By Polymerization Process | Solution Polymerization | ||

| Suspension/Inverse-Suspension Polymerization | |||

| Gel Polymerization | |||

| By Application | Baby Diapers | ||

| Adult Incontinence Products | |||

| Feminine Hygiene | |||

| Agriculture Support | |||

| Other Application | |||

| By End-User Industry | Personal Care and Hygiene Manufacturers | ||

| Agriculture Input Suppliers | |||

| Healthcare Providers | |||

| Other End-use Industries (Telecom and Power Cable Makers and Food and Pharmaceutical Cold-Chain Logistics) | |||

| Geography | Asia-Pacific | China | |

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Egypt | |||

| Nigeria | |||

| Rest of Middle-East and Africa | |||

By Product Type

| Polyacrylamide |

| Acrylic Acid Based |

| Others |

By Polymerization Process

| Solution Polymerization |

| Suspension/Inverse-Suspension Polymerization |

| Gel Polymerization |

By Application

| Baby Diapers |

| Adult Incontinence Products |

| Feminine Hygiene |

| Agriculture Support |

| Other Application |

By End-User Industry

| Personal Care and Hygiene Manufacturers |

| Agriculture Input Suppliers |

| Healthcare Providers |

| Other End-use Industries (Telecom and Power Cable Makers and Food and Pharmaceutical Cold-Chain Logistics) |

Geography

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle-East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the super absorbent polymers market?

The super absorbent polymers market size stands at 3.78 million tons in 2025 and is projected to reach 4.56 million tons by 2030.

Which application dominates global demand?

Baby diapers hold 65% of global volume, underpinned by steady births in developing countries and premiumization in mature economies.

Why are bio-based SAPs gaining traction in Europe?

EU regulations mandating recyclability and lower carbon footprints push converters toward cellulose and starch-based SAPs that offer biodegradability advantages.

Which region is growing the fastest?

North America records the highest regional CAGR at 5.50% through 2030 due to premium adult incontinence and specialty industrial applications.

How volatile are SAP raw material costs?

Acrylic acid prices can swing 25% within a single quarter, driving interest in vertical integration and alternative bio-feedstocks to stabilize margins.

Page last updated on: June 27, 2025